Advertisement

Advertisement

DAX Index Today: French Election Result and US Inflation Expectations in Focus

By:

Key Points:

- The DAX gained 0.14% on Friday, July 5, ending the session at 18,476.

- On Monday, July 8, investors will react to the French election run-off results.

- German trade data and US consumer inflation expectation numbers also need consideration.

The DAX Performance Overview

On Friday, July 5, the DAX gained 0.14%. Following a 0.41% advance on Thursday, July 4, the DAX ended the session at 18,476.

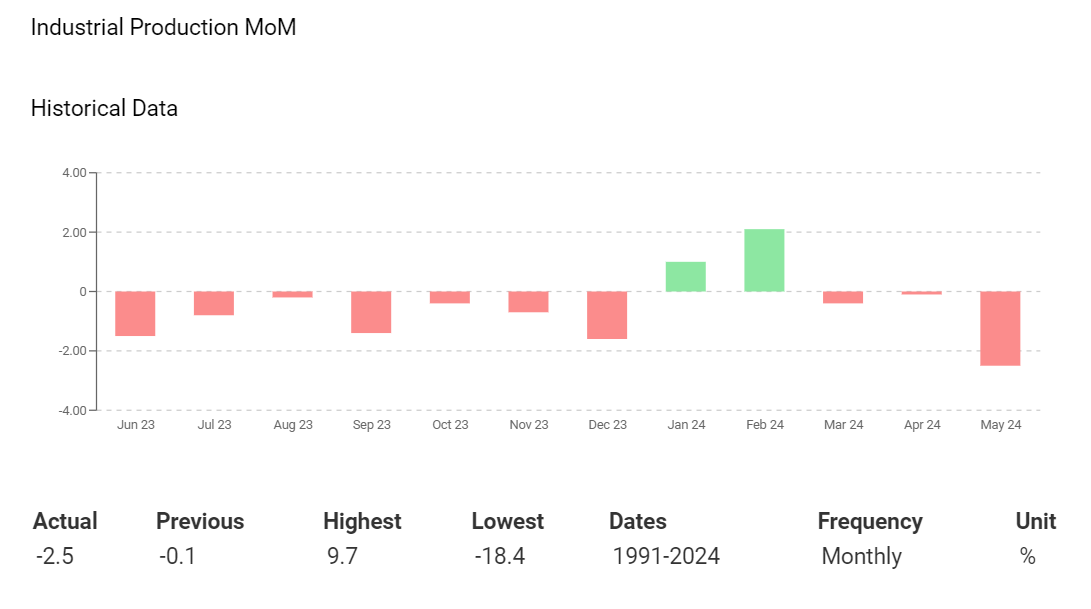

German Industrial Production Tumbles in May

On Friday, economic indicators from Germany sent more red flags. German industrial production unexpectedly slid by 2.5% in May after a revised 0.1% increase in April. The May figures raised the prospects of a German economic recession after disappointing services PMI and factory orders numbers.

For perspective, German industrial production declined for the ninth month from twelve, highlighting the weak demand environment.

A deteriorating macroeconomic environment could support investor bets on multiple ECB interest rate cuts over the remainder of the year.

Meanwhile, the US Jobs Report raised investor expectations of a September Fed rate cut.

US Wage Growth and Unemployment Rate Raise Fed Rate Cut Bets

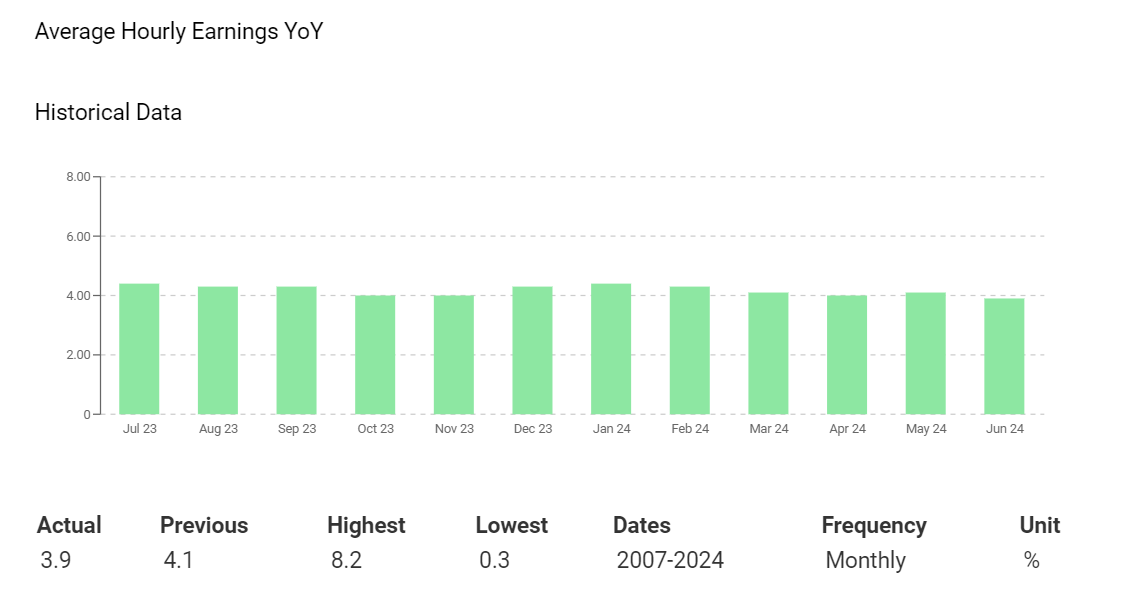

Later in the Friday session, the US Jobs Report warranted investor attention. Year-on-year, average hourly earnings slowed from 4.1% to 3.9%, while the US unemployment rate rose from 4.0% to 4.1% in June.

Investors reacted to the US Jobs Report, raising bets on a September Fed rate cut.

The softer wage growth numbers were significant. On Tuesday, July 2, Fed Chair Powell warned that wage growth remained elevated.

For perspective, average hourly earnings trended downwards in 2024, supporting a less hawkish Fed rate path. Average hourly earnings increased 4.4% in January 2024.

Nevertheless, the DAX gave up gains from earlier in the session. Uncertainty about the Sunday, July 7, French election run-off affected buyer demand for DAX-listed stocks.

The Friday Market Movers

Continental AG extended its gains from Thursday, July 4, rallying 3.76% on the company expecting strong growth in China and a likely jump in Q2 2024 profits.

Rising investor bets on a September Fed rate cut drove buyer demand for tech stocks. Infineon Technologies advanced by 2.29%, while SAP ended the day up 1.10%.

However, Deutsche Bank slid by 1.30% amid the uncertainty about the French election run-off. The possibility of disruption to the Euro area economy and destabilization of the EU Project influenced buyer demand for bank stocks.

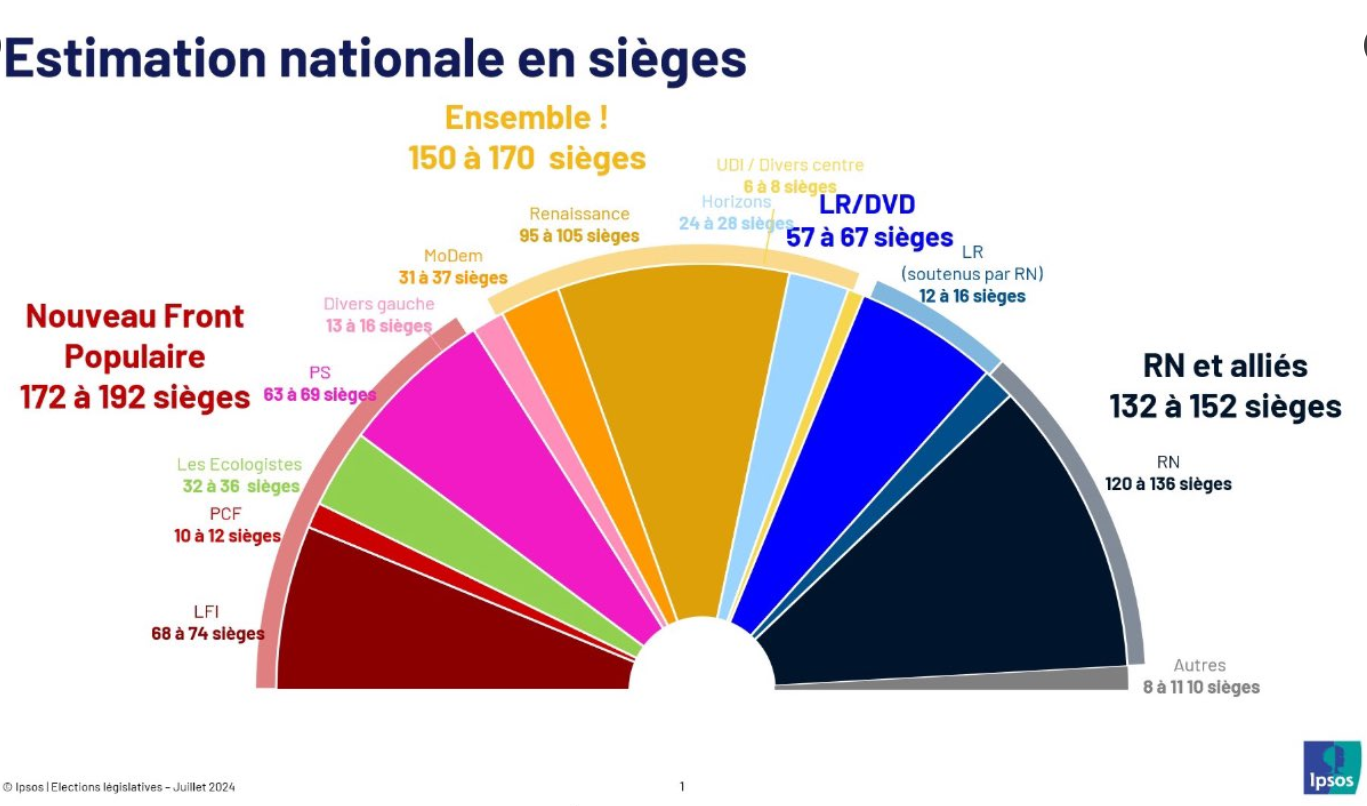

France Election Run-Off: Far Right National Rally Party in Third

On Monday, July 8, indications from the French election run-off signaled a hung French parliament. While averting a far-right National Rally Party absolute majority was positive, political gridlock could affect the French and Euro area economies.

EurAsia Group Managing Director Europe Mujtaba Rahman commented on the election results, saying,

“France has today rejected government by the Far Right, but looks likely to face months of political chaos with a blocked parliament. Surprisingly, early projections suggest that the *Left alliance* might even pip the Far Right as the largest bloc in the new National Assembly.”

Rahman also shared early projections from Ipsos that showed the far-right falling to third after leading the first round.

While a hung parliament was likely the best result, political uncertainty will again plague the European markets.

Could the far-left form a coalition government?

As the dust settles from the Sunday run-off, investors will shift focus to the German economy.

German Trade Terms:

On Monday, July 8, the German economy will face scrutiny for the third session.

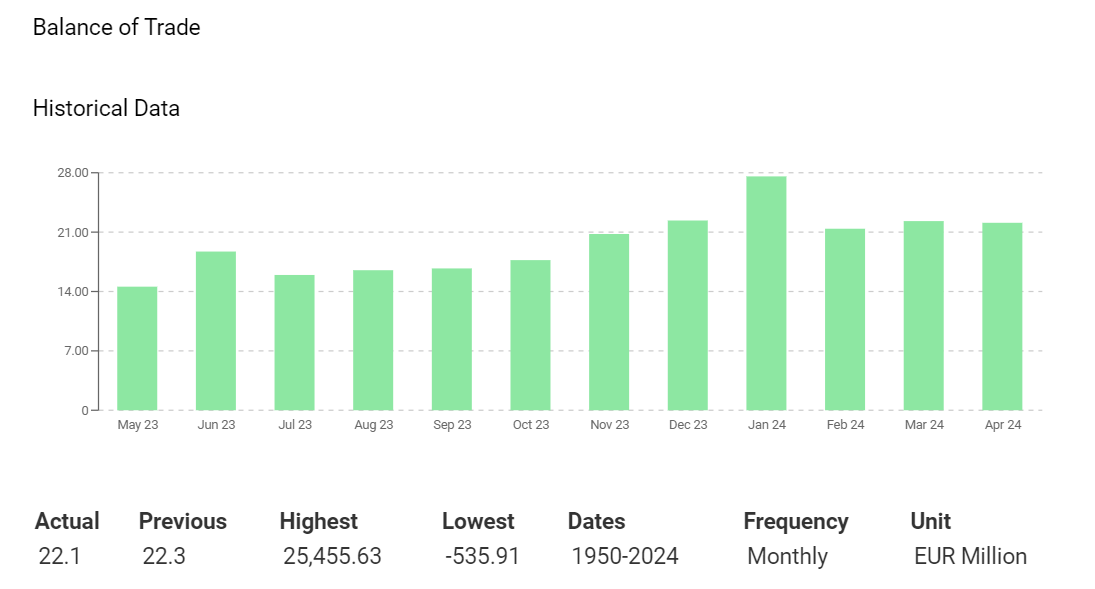

Economists forecast the German trade surplus to narrow from €22.1 billion to €20.3 billion in May.

A larger-than-expected fall in the trade surplus may signal a weakening demand environment.

For context, the German trade surplus has remained relatively steady in recent months. Nevertheless, demand remains a concern after the recent German factory order and industrial production numbers. The German trade surplus stood at a 12-month high of $27.57 million in January 2024.

While the numbers will attract investor attention, US inflation data may impact market risk sentiment more.

Can US consumer inflation expectations distract the European markets from the French election results?

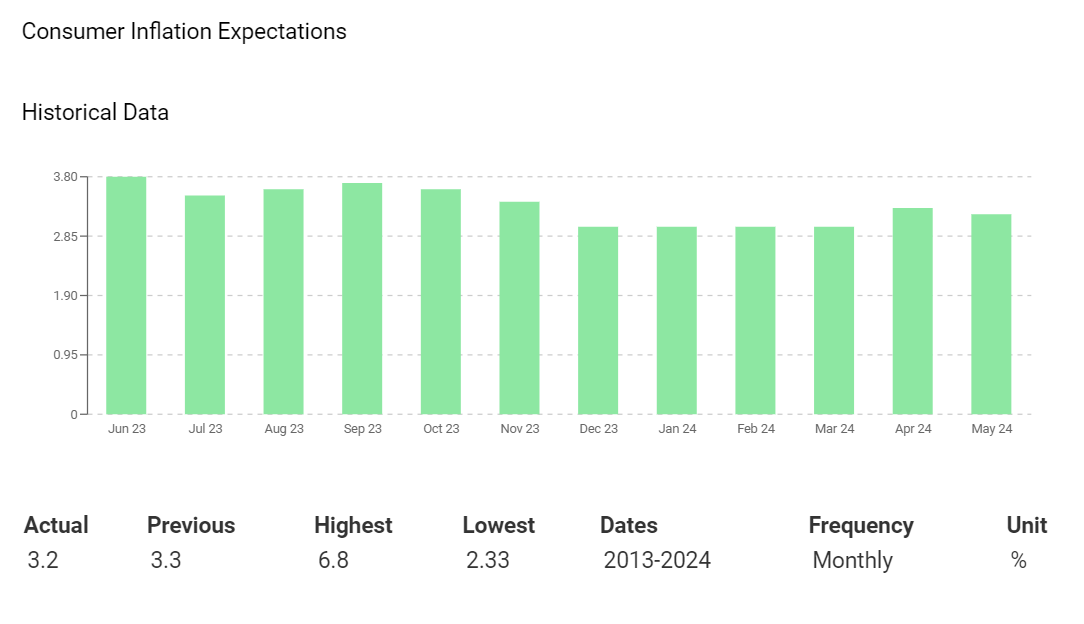

US Consumer Inflation Expectations: A Headline Inflation Predictor

Later in the session on Monday, US consumer inflation expectations could affect investor expectations of a September Fed rate cut.

Economists forecast consumer inflation expectations to fall from 3.2% to 3.0% in June.

Downward trends in consumer inflation expectations could signal a fall in consumer spending. Consumers delay plans to purchase goods and services if they expect consumer prices to fall. Downward trends in consumer spending could dampen demand-driven inflation and allow the Fed to cut interest rates.

For perspective, consumer inflation expectations rose to a June 2022 high of 6.8% before falling to 3.0% in December 2023.

Softer-than-expected consumer inflation expectations may fuel buyer demand for riskier assets, including DAX-listed stocks.

Near-Term Outlook

Near-term trends for the DAX will hinge on French election-related updates and US inflation numbers. While softer US inflation figures could fuel buyer appetite for DAX-listed stocks, a far-left government could spook investors.

On the Futures markets, the DAX was up by 12 points, while the Nasdaq mini declined by 32 points.

In conclusion, the French Election-related news requires investor consideration after the Sunday run-off. A far-left government could adversely impact buyer appetite for riskier assets. However, US inflation numbers could support bets on a September Fed rate cut and cushion the downside from Euro area geopolitical risks.

Investors should remain vigilant. Monitor the news wires, real-time economic data, and expert commentary to manage trading strategies accordingly. Stay informed with our latest updates and insights to navigate the equity markets.

To better navigate these market conditions, understanding the technical indicators for the DAX is crucial. Here is a look at the key technical levels and trends.

DAX Technical Indicators

Daily Chart

The DAX remained comfortably above the 50-day and 200-day EMAs, affirming the bullish price signals.

A DAX break above the 18,500 handle could support a move toward the 18,750 handle.

The French Election-related news, German trade data, and US inflation figures need consideration.

Conversely, a DAX break below the 50-day EMA could signal a fall to 18,000. A drop below 18,000 could give the bears a run at the 17,615 support level.

The 14-day RSI at 55.29 suggests a return to the 18,750 handle before entering overbought territory.

4-Hourly Chart

The DAX held above the 50-day and 200-day EMAs, confirming the bullish price trends.

A return to 18,500 could give the bulls a run at the 18,750 handle.

However, a DAX drop below the 50-day and 200-day EMAs could signal a fall to the 18,000 handle.

The 14-period 4-hour RSI at 58.76 indicates a DAX rise to 18,750 before entering overbought territory.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement