Advertisement

Advertisement

Hang Seng Declines as Trump Election Hopes Stir Tariff Worries for China

By:

Key Points:

- Aussie inflation eases, testing RBA rate cut hopes for Q4 2024 as CPI nears RBA’s 2-3% target band in September.

- Hang Seng and Mainland markets drop amid Trump tariff concerns and Beijing’s lack of fresh stimulus measures.

- Nikkei rises 0.94% on BoJ hold expectations post-election as the weaker yen boosts export-oriented stocks.

In this article:

US Markets: Nasdaq Extends Winning Streak to Four Sessions

On Tuesday, October 29, US equity markets had a mixed session. The Nasdaq Composite Index extended its winning streak to four sessions, advancing by 0.78%, with the S&P 500 gaining 0.16%. However, the Dow declined by 0.36%.

During the US session, Cadence Design Systems (CDNS) raised its 2024 profit outlook, contributing to the Nasdaq’s gains. In after-hours trading, Alphabet Inc. (GOOGL) jumped by 5.88% after beating earnings expectations.

US Economic Indicators Boost Bets on December Fed Rate Cut

On Tuesday, JOLTS job openings and consumer confidence figures raised investor expectations for 25-basis point Fed rate cuts in November and December.

JOLTS job openings dropped from 7.861 million in August to 7.443 million in September. A weaker labor market may curb consumer spending, dampening demand-driven inflation. However, the CB Consumer Confidence Index increased from 99.2 in September to 108.7 in October, supporting expectations for a soft US economic landing.

According to the CME FedWatch Tool, the chances of a 25-basis point December Fed rate cut increased from 69.9% on October 28 to 78.3% on October 29.

Aussie Inflation Tests RBA Rate Cut Expectations

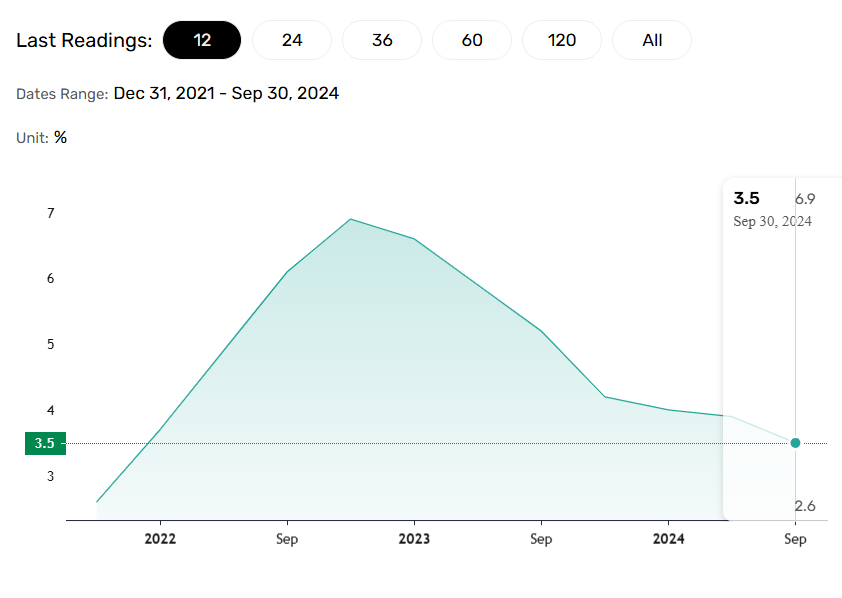

On Wednesday, October 30, Aussie inflation figures impacted expectations for a Q4 2024 RBA rate cut. The Monthly CPI Indicator dropped from 2.7% in August to 2.1% in September, nearing the bottom band of the RBA’s 2-3% target range. However, underlying inflation eased from 3.9% in Q2 2024 to 3.5% in Q3 2024, remaining above the target range, potentially delaying a rate cut until next year.

Potential for Fresh US Tariffs on China Grows

This week, markets raised expectations for a Trump second term, boosting demand for US stocks.

The latest national polls show Kamala Harris leading Trump by just 1.4 points. However, Trump’s foreign policy stance could also impact China’s economy if punitive tariffs are reintroduced. The timing of tariffs could be crucial as China grapples with deflationary pressures and a weakening economy.

Hang Seng and Mainland China Equities Slip Amid Uncertainty

In Asian markets, the Hang Seng Index declined by 0.46% on Wednesday morning. Concern about a Trump win and a lack of fresh stimulus measures from Beijing impacted demand for Hong Kong and Mainland China-listed stocks.

The Hang Seng Tech Index declined by 0.59%, with tech giants Alibaba (9988) and Baidu (9888) seeing losses of 1.13% and 1.05%, respectively.

Mainland China’s equity markets also trended lower in the morning session, with the CSI 300 and the Shanghai Composite falling 0.11% and 0.09%, respectively.

Nikkei Advances Amid Political Standoff

In Japan, the Nikkei Index rallied 0.94% on Wednesday morning. The political standoff after Sunday’s general election in Japan tempered investor bets on a Q4 2024 Bank of Japan rate hike.

The shift in sentiment toward the BoJ rate path eased demand for the Japanese Yen. Notably, the USD/JPY pair continued to hold onto the 153 handle, supporting demand for Nikkei Index-listed export stocks. However, tech stocks led the gains as investors reacted to overnight US earnings results.

Key movers included SoftBank Group Corp. (9984), which advanced by 2.25%. Tokyo Electron gained 0.88%, while Sony Group Corp. (6758) was up 1.62% in the morning session.

ASX 200 Falls on RBA Rate Path Shifts

The ASX 200 Index declined by 0.44% on Wednesday morning. Banking stocks led the Index into negative territory, while gold, mining, and tech stocks limited the losses.

Commonwealth Bank of Australia (CBA) and National Australia Bank (NAB) saw losses of 1.02% and 1.11%, respectively.

However, mining giants BHP Group Ltd (BHP) and Rio Tinto Ltd (RIO) advanced by 1.18% and 0.69%, respectively, as iron ore spot prices gained ground overnight. Northern Star Resources (NST) gained 1.84% as the gold spot price struck an all-time high of $2,782 on Wednesday.

Looking Ahead

Investors should remain vigilant. Fiscal stimulus-related news from China, targeting consumer spending could drive demand for HK and Mainland China-listed stocks.

However, central bank commentary and election-related news from Japan also require consideration. Rising expectations of a BoJ monetary policy hold through Q4 2024 could impact the Yen, potentially fueling demand for Nikkei Index-listed stocks.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement