Advertisement

Advertisement

MicroStrategy’s $42 Billion BTC Purchase Plan Will Likely Face Headwinds

By:

Key Points:

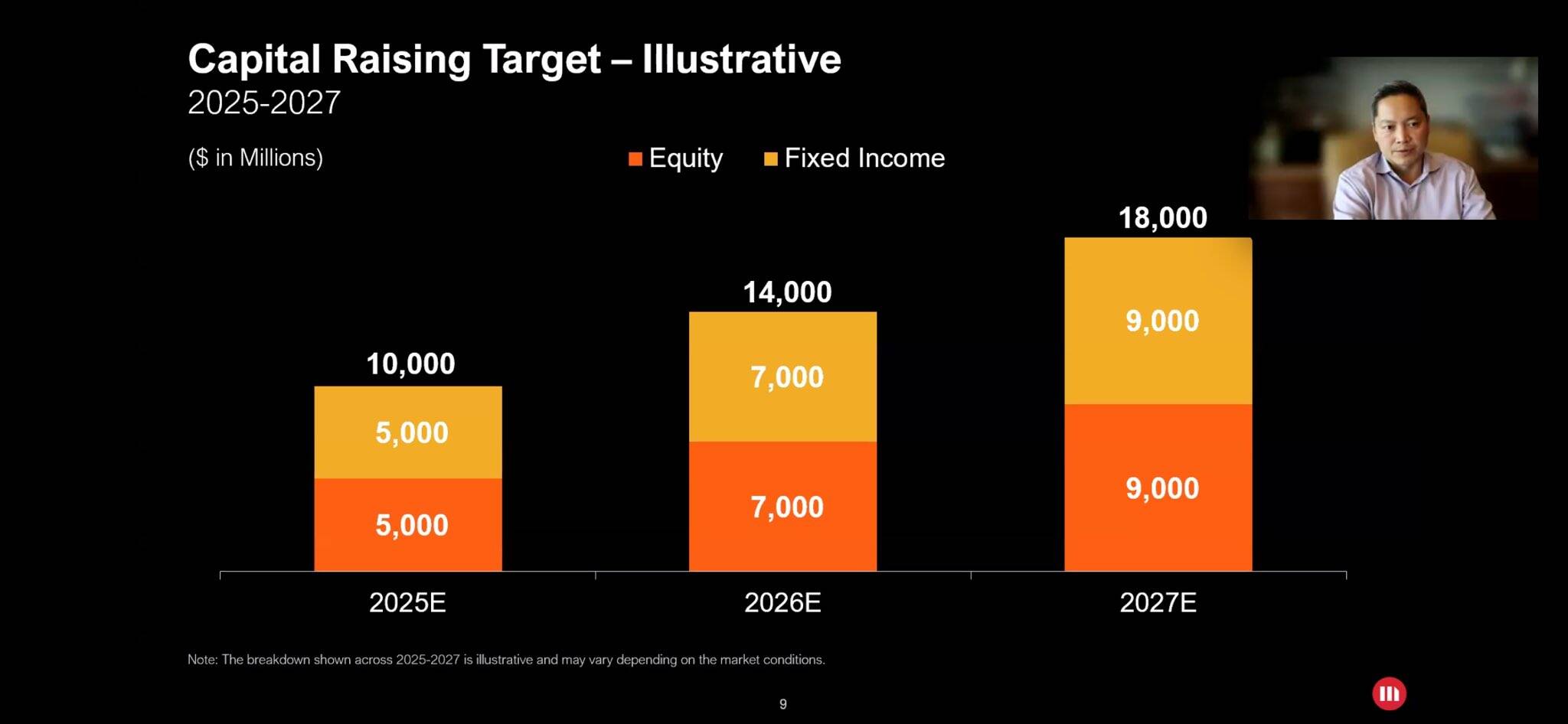

- MicroStrategy’s "21/21 Plan" aims to invest $42 billion in Bitcoin over three years, funded equally through equity and fixed-income.

- Declining SaaS revenue raises concerns about the company’s ability to sustain debt payments without tapping into Bitcoin holdings.

- With MSTR’s high premium over Bitcoin’s market value, direct Bitcoin purchase may be a more cost-effective investment strategy.

In this article:

Business intelligence firm MicroStrategy (MSTR) will purchase $42 billion worth of Bitcoin (BTC) tokens in the next three years through a mix of equity and fixed-income securities.

During the Nasdaq firm’s third-quarter earnings call on Oct. 30, it said it would raise $21 billion of equity and $21 billion of fixed-income securities—a so-called “21/21 Plan”—to invest solely in the top-ranking cryptocurrency.

Can MicroStrategy Raise More Capital For Bitcoin Purchases in The Future?

MicroStrategy has repositioned itself as a “Bitcoin development company” alongside its core SaaS business, actively acquiring Bitcoin to enhance shareholder value.

The firm funds these acquisitions through debt issuance, share sales, and operational cash flows. However, with minimal cash flow from SaaS in recent quarters, MicroStrategy has relied increasingly on capital markets to fuel its Bitcoin purchases.

As of its Q3 earnings report, MicroStrategy holds approximately $17.3 billion in Bitcoin, with about $4.2 billion in long-term debt. Notably, the company is focused on servicing its debt through revenue rather than liquidating its Bitcoin holdings.

In the past 12 months, MicroStrategy has paid around $50 million in interest, exceeding its profit for the same period. Over the next year, it anticipates an additional $35 million in interest expenses.

In Q3, MicroStrategy reported annualized sales of around $480 million, with losses now slightly over $200 million. It shows that the firm’s top-line sales are not growing.

On the other hand, its top SaaS rivals, including Palantir (PLTR), ServiceNow (NOW), and Datadog (DDOG), have reported year-over-year growth in the 20-30% range.

Lowering revenues raises the risk of MicroStrategy relying on ‘other’ methods to meet its debt obligations to bondholders. That may involve launching Bitcoin-related businesses, with its founder and executive chairman, Michael Saylor, proposing to launch a Bitcoin Bank.

If not, the firm may have no other method to repay its bondholders but to secure its Bitcoin profits, which may stress the crypto market.

Should You Buy MSTR Stock to Gain Exposure in Bitcoin?

MicroStrategy’s current valuation is around $47 billion, comprising its $17.3 billion worth of Bitcoin holdings and a breakeven operating segment.

The firm’s convertible notes allow external investors to gain indirect Bitcoin exposure via MSTR stock. However, this approach has diluted existing shareholders, with much of the premium stemming from MicroStrategy’s leveraged Bitcoin accumulation strategy.

Given signs that this momentum may slow in the coming quarters, paying nearly $190,000 per Bitcoin (reflecting MSTR’s 176% premium over its holdings’ market value) seems increasingly unjustified.

Instead, it looks wiser to buy Bitcoin directly.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement