Advertisement

Advertisement

U.S. Q1 GDP Contracts 0.2% as Jobless Claims Spike, Corporate Profits Slide $118B

By:

Key Points:

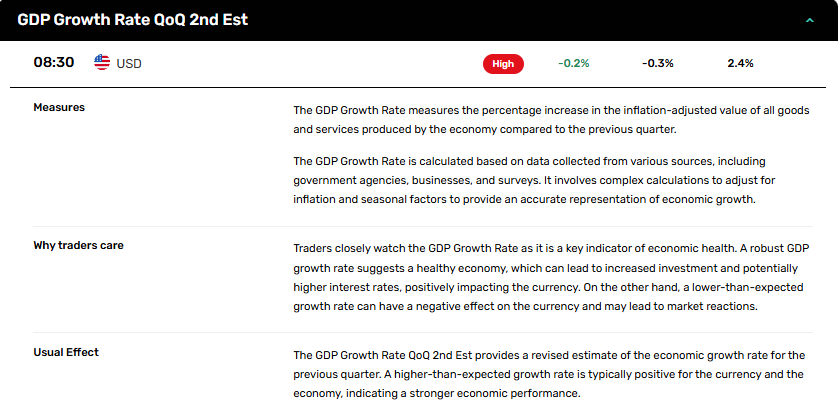

- U.S. GDP contracted 0.2% in Q1 2025, missing flat-growth estimates and highlighting a sharp slowdown from Q4's 2.4% gain.

- Jobless claims rose to 240,000, with continued claims hitting 1.92M—the highest level since late 2021.

- Corporate profits dropped $118B in Q1, a sharp reversal from Q4’s $204.7B rise, signaling early earnings pressure.

GDP Contracts, Corporate Profits Slide as Labor Market Loosens

U.S. economic momentum cooled sharply in Q1 2025, with real GDP declining at an annual rate of 0.2%, according to the Bureau of Economic Analysis’ second estimate. This is a modest upward revision from the initial -0.3% figure but still fell below consensus expectations, which had anticipated flat growth. The updated reading highlights a significant pullback from the 2.4% expansion recorded in Q4 2024.

Imports Surge, Government Spending Drops: What Dragged GDP Lower?

The GDP contraction was led by a sharp increase in imports and a reduction in government spending—both acting as key drags. The revision reflected stronger-than-expected investment, particularly in private inventories, but that was more than offset by weaker consumer spending, notably in healthcare and recreational services. Final sales to private domestic purchasers were revised down to 2.5% from 3.0%, pointing to weaker internal demand than originally reported.

Corporate Profits Miss Expectations with $118B Decline

Preliminary Q1 corporate profits fell by $118.1 billion, contrasting with a $204.7 billion gain in Q4. This result came in weaker than market expectations, signaling early earnings strain. Inventory valuation adjustments in sectors like chemical manufacturing helped limit the downside, but declines in wholesale trade and recreational goods dragged overall profits.

The report will likely raise concerns over future earnings resilience, particularly for sectors tied to consumer discretionary and trade-sensitive industries.

Unemployment Claims Surge to 240,000—Labor Cooling Faster Than Forecast

Weekly initial jobless claims jumped to 240,000 for the week ending May 24, exceeding estimates near 230,000. The 4-week moving average dipped slightly to 230,750, but continued claims climbed to 1.92 million—the highest since November 2021. Insured unemployment rose to 1.3%, also above expectations. States such as Illinois and Indiana reported higher layoffs in manufacturing and construction, while Michigan and Virginia showed notable declines, signaling uneven but broad-based labor weakness.

Inflation Holds Steady but Above Target—Fed Dilemma Persists

The PCE price index remained unchanged at 3.6%, while the core PCE was revised slightly lower to 3.4%. Both readings are still well above the Federal Reserve’s 2% inflation target, complicating policy expectations. Although the inflation data was largely in line with forecasts, the persistence of elevated core inflation alongside weaker growth reinforces concerns over stagflation risk.

Market Forecast: Bearish Bias Builds on Weak Growth and Profit Miss

With GDP below estimates, corporate profits under pressure, and jobless claims rising above forecasts, traders face a bearish near-term outlook. Equities may come under renewed selling pressure, especially in sectors with weak earnings visibility. Treasury markets could benefit from safety bids, while the dollar may gain support from risk-off positioning. Inflation stickiness, however, may limit the Fed’s policy flexibility, adding another layer of complexity to the trading environment.

About the Author

James HyerczykProfits & Punchlines

Mr.Hyerczyk is a technical analyst, market researcher, educator and trader. Jim is an expert in the area of patterns, price and time analysis, Forex and stocks.

Advertisement