Advertisement

Advertisement

Dax Index News: Election Results Boost Outlook, But Analysis Remains Cautious

By:

Key Points:

- DAX dropped 0.12%, closing at 22,288, amid cautious investor sentiment ahead of Germany's snap elections.

- EUR/USD rallied 0.55% and DAX futures surged 251 points as Friedrich Merz secured the German chancellorship.

- DAX eyes record high of 22,935 as election jitters subside. However, US tariff threats continue to fuel uncertainty.

DAX Edges Lower Amid German Election Uncertainty

The DAX declined by 0.12% on Friday, February 21, following Thursday’s 0.53% loss, closing at 22,288.

Investors turned cautious as Germany’s snap elections on February 23 loomed.

Sector Highlights: Autos and Banks Cushion the Losses

Auto and bank stocks limited Friday’s losses. Volkswagen rallied 1.62%, while Porsche advanced by 0.98%. However, Mercedes-Benz Group fell 1.39% as investors continued responding to disappointing earnings results and a dividend cut.

Deutsche Bank gained 1.40% after Standard Chartered Bank reported a jump in annual profits and announced a share buyback.

In contrast, Airbus SE and MTU Aero Engines AG extended their losses from Thursday after Airbus had warned about a challenging production outlook and A350 freighter delays.

Germany’s Private Sector Contracts More Slowly

Germany’s February private sector PMI data signaled a modest improvement in private sector activity. A less marked contraction across the manufacturing sector supported an increase in the Composite PMI to 51.0 in February, up from 50.8 in January.

However, the PMI data had a limited impact on risk sentiment, with the weekend’s election in focus.

German Business Sentiment and DAX Outlook

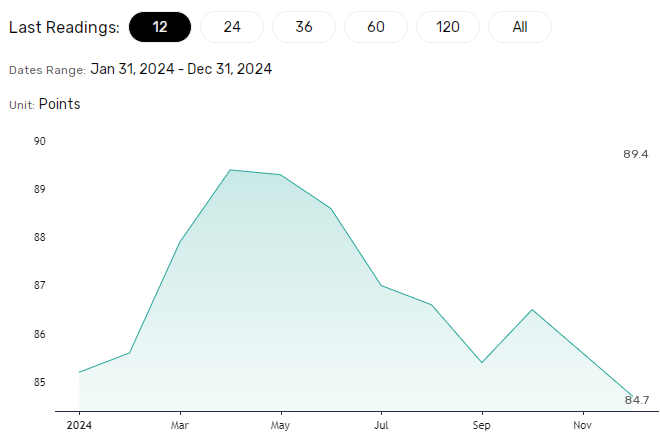

On Monday, February 24, Germany’s Ifo Business Climate numbers require consideration. Economists expect the Index to rise from 85.1 in January to 85.8 in February. Improving business sentiment could signal job creation and higher wages, fueling consumption and inflation.

However, the numbers are unlikely to influence the ECB rate path unless the Index nears April and May 2024’s higher 89-90 range.

Finalized Eurozone inflation figures are also out later today. However, barring a marked revision, the numbers are unlikely to impact risk assets.

German Election Results Bring Relief but Concerns Remain

On Sunday, February 23, Germany’s election results delivered no shocks, with conservative Friedrich Merz set to become the new Chancellor. Merz pledged to reduce EU dependence on the US ahead of coalition negotiations.

Markets reacted positively: the EUR/USD rallied 0.55% to 1.05137, and the DAX futures jumped 251 points ahead of Monday’s European opening bell.

Expert Views on the German Election Results: Bad But Could Be Worse!

Despite the positive market reaction, experts expressed concerns. Robin Brooks, Senior Fellow at the Brookings Institute, commented:

” Today’s election is a disaster for Germany. CDU underperforms and goes weakened into coalition negotiations with SPD and Greens, who undermined CDU’s efforts to restrict immigration and take votes away from AfD. Deeply cynical electioneering by SPD and Greens that only helps AfD.”

A Jamaica coalition comprising CDU/SPD/Greens could allow the AfD to continue growing and have a greater presence in the next election.

However, things could have been worse. Brooks acknowledged:

“It could have been worse, you are right. AfD is also – along with CDU – underperforming expectations when you take into account the string of attacks in the run-up to the election. Hopefully a sign that most Germans are still moderate and not panicking…”

US Services Sector Contracts as Inflation Returns

Meanwhile, in the US, weaker-than-expected services data weighed on risk assets.

The S&P Global Services PMI slid unexpectedly from 52.9 in January to 49.7 in February, signaling a sector contraction. Accounting for around 80% of the US economy, February’s numbers could support a more dovish Fed rate path.

However, the Michigan Inflation Expectations Index jumped from 3.3% in January to 4.3% in February, potentially delaying Fed rate cuts.

The Kobeissi Letter commented on US inflation, stating:

“US CPI inflation is on track to hit 4.6% over the next 6 months, according to Bank of America. CPI inflation has averaged +0.4% on a month-over-month basis over the last 3 months. If this trend continues, this puts year-over-year inflation on pace to hit 4.6% by July, the highest since April 2023.”

These projections underscored the increasing uncertainty about the Fed rate path amid ongoing concerns about tariffs.

US Markets Tumble on Economic Data

US equity markets tumbled on Friday, February 21, as investors digested the service sector and inflation numbers. The Nasdaq Composite Index dropped by 2.20%, while the Dow and the S&P 500 saw losses of 1.69% and 1.71%, respectively.

Key Focus: Dallas and Chicago Fed Reports

On February 24, the Chicago Fed National Activity and Dallas Fed Manufacturing Indexes will draw interest.

After Friday’s services sector data, better-than-expected figures could ease fears of a sharp economic slowdown, potentially boosting risk sentiment. Conversely, weaker readings could exacerbate concerns of a slowdown.

Near-Term Outlook

The DAX’s direction hinges on German election-related updates, tariff developments, and central bank guidance.

- Progress toward a conservative-led coalition, easing tariff risks, and dovish central bank guidance could push the DAX above 22,500.

- Coalition stumbling blocks, rising tariff threats, and a hawkish Fed may pull the Index toward 22,000.

As of Friday morning, US futures also indicated a positive start, with the Nasdaq 100 mini up 96 points.

DAX Technical Indicators

Daily Chart

Despite last week’s losses, the DAX sits well above the 50-day and 200-day Exponential Moving Averages (EMAs). While holding above key moving averages, rising volatility suggests potential short-term downside risks within the broader uptrend.

A break above 22,500 could bring the February 19 record high of 22,935 into sight. A return to 22,935 may signal a move through 23,000 next.

Conversely, if the DAX breaks below 22,150, the 22,000 level will be the next key support level.

With the 14-day Relative Strength Index (RSI) at 62.27, the DAX could return to the record high of 22,935 before entering overbought territory (RSI higher than 70).

Conclusion: Key Drivers to Watch

Traders should closely monitor:

- German political negotiations

- ECB and Fed commentary.

- Tariff policy.

Further detailed analysis of global market influences on the DAX is available here.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement