Advertisement

Advertisement

Dax Index News: German Trade Surplus Rises, but US Jobs Report Looms

By:

Key Points:

- DAX edges higher on Friday, February 7 as investors brace for US Jobs Report.

- Germany’s trade surplus widens to €20.7B, with EU exports surging 5.9% despite weaker shipments to the US.

- US labor data hints at a slowing job market—will softer wage growth fuel a dovish Fed and drive DAX higher?

DAX Opens Higher Ahead of US Jobs Report

The DAX Index opened higher on Friday, February 7, edging 0.01% to 21,905. Investors turned cautious ahead of the crucial US Jobs Report, which could influence the Fed’s policy outlook.

Sector Performance: Auto Stocks Under Pressure

Auto stocks advanced at the opening bell. Porsche advanced by 0.16%, while Volkswagen gained 0.04 %. Mercedes-Benz and BMW also advanced on US-EU trade sentiment.

German Trade and Industrial Production Send Mixed Signals

Germany’s industrial production fell 2.4% in December after a 1.5% increase in November. However, the pullback may not signal a sustained slowdown as factory orders surged 6.9% in December.

Meanwhile, Germany’s trade surplus widened from €19.7 billion to €20.7 billion in December. Exports increased by 2.9% after rising 2.1% in November.

December’s report revealed key trends:

- Exports to the US declined by 3.5%, while exports to China increased by 1.4%.

- Imports from the US rose 3.0%, while imports from China fell 1%.

- Exports to EU countries jumped 5.9%.

December’s trade data could set the stage for positive US-EU trade negotiations as tariff risks loom.

US Markets Recap

On Thursday, February 6, US equity markets posted mixed results. The Nasdaq Composite Index and S&P 500 posted gains of 0.19% and 0.39%, respectively, while the Dow dropped by 0.28%.

Notable movers included Honeywell (HON), which declined by 5.64%. The firm announced plans to break into three companies, impacting the stock price. Despite earnings beating estimates, the company’s full year guidance weighed on the stock.

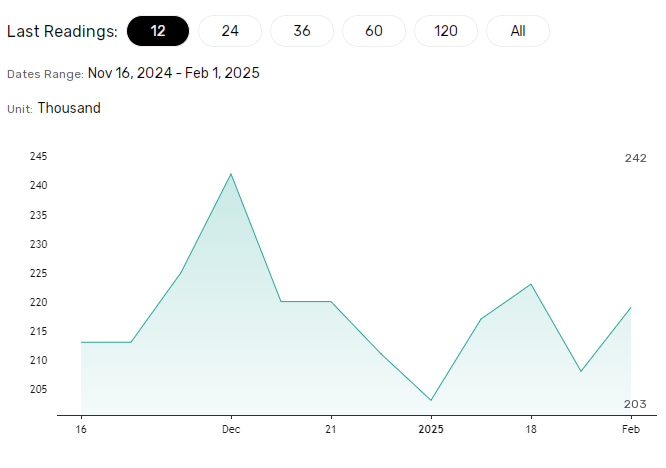

Meanwhile, US labor market data raised hopes for a less hawkish Fed rate path. Initial jobless claims rose to 219k (week ending February 1), up from 208k (week ending January 25). A softening labor market may weaken wage growth, potentially curbing consumer spending and easing inflationary pressures.

All Eyes on US Jobs Data: Will the Fed Shift Gears?

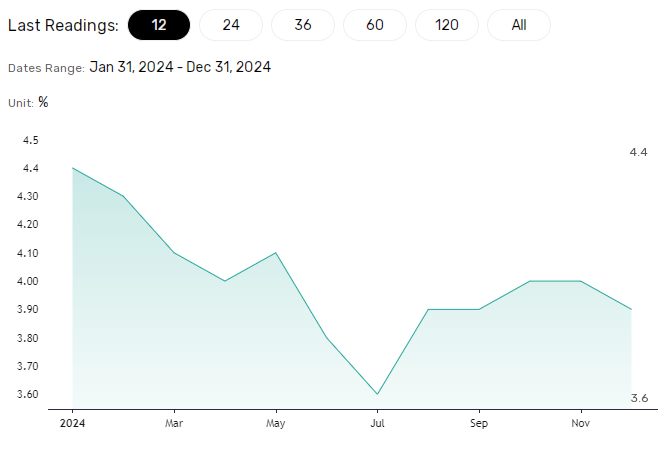

Friday’s US Jobs Report will likely influence sentiment toward the Fed rate path. Economists forecast the unemployment rate will remain at 4.1% in December. Additionally, average hourly earnings are expected to rise 3.8% year-on-year, down from 3.9% in November.

- Weaker wage growth and higher unemployment could fuel speculation about an H1 2025 Fed rate cut. A more dovish Fed rate path may lower borrowing costs, boosting company earnings, potentially driving the DAX to record highs.

- Conversely, an unexpected fall in unemployment and higher wages would likely impact rate cut hopes and weigh on the DAX.

Near-Term Outlook

The DAX’s trajectory hinges on the US Jobs Report and central bank guidance.

- A weaker-than-expected US jobs report and dovish Fed rhetoric could boost risk appetite, potentially driving the DAX above 22,000.

- Tighter US labor market conditions and hawkish Fed guidance may pull the DAX toward 21,500.

Beyond the data, investors should track US-China and EU trade developments, which will be crucial for risk sentiment. A de-escalation in trade tensions could fuel demand for risk assets, while an escalation may drag the DAX lower.

As of Friday morning, US futures pointed to a testy session, with the Nasdaq 100 mini dropping 18 points.

DAX Technical Indicators

Daily Chart

After Thursday’s 1.47% rally, the DAX remains well above the 50-day and 200-day Exponential Moving Averages (EMAs), affirming bullish price signals.

If the DAX breaks above Thursday’s record high of 21,921, the Index could move through the 22,000 threshold. A breakout from 22,000 could enable the bulls to target 22,350.

Conversely, a DAX drop below 21,750 may bring 21,500 into play. A break below 21,500 could signal a fall toward 21,000.

With the 14-day Relative Strength Index (RSI) at 74.37, the DAX remains in overbought territory (RSI higher than 70). Selling pressure may intensify if the DAX approaches the resistance level of 21,921.

Final Thoughts

The interplay between US labor market trends, central bank policy decisions, and geopolitical trade dynamics will be pivotal in determining the DAX’s near-term trajectory.

Stay ahead with our latest insights and real-time analysis here.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement