Advertisement

Advertisement

Dax Index News: Market Rallies on Ukraine Peace Hopes – Outlook and Analysis

By:

Key Points:

- DAX jumps 1.22% on Ukraine peace hopes, but potential US tariffs on autos and semiconductors pose risks to German equities.

- Germany’s inflation slows to 2.3%, fueling ECB rate cut bets that could boost borrowing and corporate earnings.

- Market eyes US jobless claims and inflation trends—soft data may drive DAX toward 22,500, while strong data could pull it lower.

“I just spoke to President Volodymyr Zelenskyy of Ukraine. The conversation went very well. He, like President Putin, wants to make PEACE. We discussed a variety of topics having to do with the War, but mostly, the meeting that is being set up on Friday in Munich, where Vice President JD Vance and Secretary of State Marco Rubio will lead the Delegation.”

Sector Performance: Auto Stocks Shine

Auto stocks led the gains on February 13. BMW soared 4.25%, while Volkswagen and Mercedes-Benz Group rallied 3.86% and 3.53%, respectively. Porsche also advanced at the open.

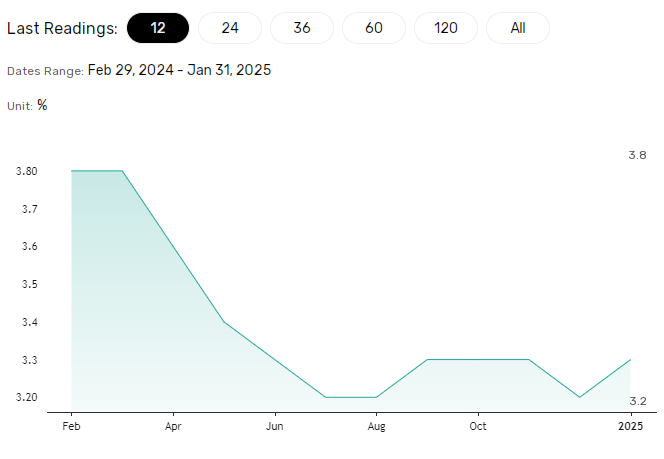

German Inflation Cools, Boosting Multiple ECB Rate Cut Bets

Germany’s annual inflation rate eased from 2.6% in December to 2.3% in January. While holding above the ECB’s 2% target, the slowdown could raise confidence among policymakers that inflation is on a sustainable path toward the target.

The timing is significant as the EU faces potential US tariffs on its goods amid a fragile economic backdrop. Lower borrowing costs could boost consumer credit demand and consumption. For German listed stocks, lower borrowing costs may increase earnings and valuations.

Expert Views on Disinflation and the ECB Policy Outlook

Daniel Kral, a macro specialist covering Europe for Oxford Economics, commented on potential hurdles to disinflation and the ECB’s policy outlook:

“Despite large cuts to gas consumption since 2022, the EU is still at the mercy of the weather with the current cold spell draining storages. Current futures imply gas prices averaging 75% higher in 2025 than last year. Not good news re disinflation and monetary policy easing.”

US Markets Recap

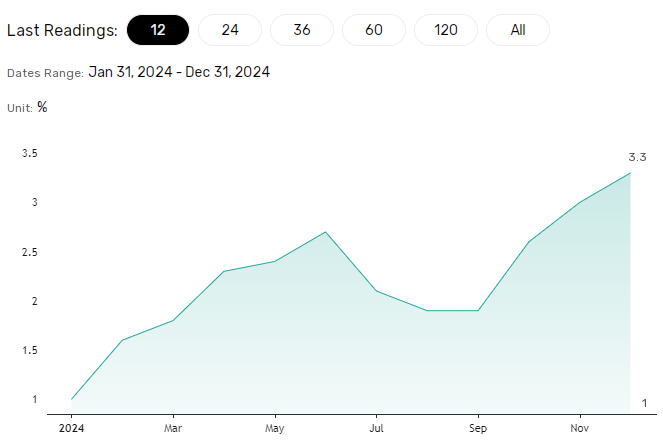

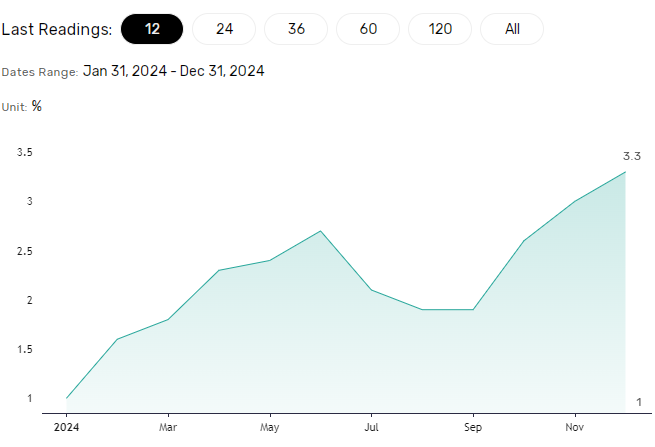

On Wednesday, February 12, US equity markets struggled as investors assessed the impact of US inflation figures on the Fed rate path. The Nasdaq Composite Index edged 0.03% higher, while the Dow and S&P 500 dropped by 0.50% and 0.27%, respectively.

The US core inflation rate unexpectedly rose from 3.2% in December to 3.3% in January, above forecasts of 3.1%.

January’s CPI Report preceded Fed Chair Powell’s second day of testimony on Capitol Hill. Powell remarked on the inflation numbers, stating:

“We’re not quite there yet.”

January’s inflation numbers and Powell’s comments sank bets on multiple Fed rate cuts in 2025. Markets now expect a September rate cut at the earliest after previously pricing in June and Q4 2025 Fed moves.

In the bond markets, 10-year US Treasury yields surged to a session high of 4.66% before easing back.

How Will US Data Impact Risk Assets?

US producer prices and labor market data will give traders more clues about the demand environment and potential consumer price trends.

Economists expect producer prices to increase 3.4% year-on-year in January, up from 3.3% in December. A higher reading could further reduce bets on an H1 2025 Fed rate cut, potentially impacting risk assets. Conversely, softer producer prices may revive hopes of a near-term Fed rate cut.

The January figures are significant as traders consider producer prices a leading inflation indicator. In a rising demand environment, producers pass higher costs on to customers, while producers pass on cost savings if demand wanes.

Economists forecast that initial jobless claims will drop to 215k (week ending February 8), down from 219k (week ending February 1).

A larger-than-expected drop could signal a tighter labor market, potentially fueling wage-driven inflation. Conversely, an unexpected spike may overshadow producer price trends, supporting a more dovish Fed rate path.

Near-Term Outlook

The DAX’s near-term trajectory hinges on upcoming US inflation and labor market data.

- Softer producer prices and higher jobless claims could boost demand for rate-sensitive stocks, potentially pushing the DAX above 22,500.

- Higher-than-expected producer prices and a sharp drop in claims may drag the DAX toward 22,350.

Beyond US data, geopolitical risks and trade developments require consideration. An escalation in US-EU trade tensions could pressure the DAX, while a de-escalation may drive the Index to record highs. However, progress toward an end to the Ukraine war could counter tariff concerns in the near term.

As of Thursday morning, US futures pointed to a positive session, with the Nasdaq 100 mini rising 102 points.

DAX Technical Indicators

Daily Chart

After Thursday morning’s breakout, the DAX sits well above the 50-day and 200-day Exponential Moving Averages (EMAs), affirming bullish price signals.

If the DAX surpasses Thursday’s record high of 22,430, it could move toward 22,500. A breakout from 22,500 may allow the bulls to target 22,750 next.

Conversely, a DAX drop to 22,350 could bring 22,150 into play.

With the 14-day Relative Strength Index (RSI) at 78.73, the DAX remains in overbought territory (RSI higher than 70). Selling pressure may intensify if the DAX approaches the key resistance level of 22,430.

Final Thoughts

The DAX’s outlook depends on US economic indicators, central bank forward guidance, geopolitics, and tariff developments.

Stay ahead with our latest insights and real-time analysis here.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement