Advertisement

Advertisement

Gold Set to Shine as OECD Flags Policy Risk and Negative Real Rates

By:

Key Points:

- OECD cuts U.S. growth forecast to 1.6% for 2025, raising stagflation concerns and complicating Fed rate policy outlook.

- Rising inflation projections up to 4% may force the Fed to keep rates higher, delaying expected easing in 2025.

- Treasury yields face conflicting pressures from weak growth and persistent inflation, flattening the yield curve.

OECD Cuts U.S. Growth Forecast: Will the Fed Tighten Despite Slowdown?

A sharp downgrade in U.S. growth expectations by the OECD is sending ripples through global markets, raising the stakes for Federal Reserve policy while reshaping outlooks across Treasuries, the dollar, gold, and equities. The group now projects U.S. GDP will rise just 1.6% in 2025, down from 2.2%, and only 1.5% in 2026, reflecting growing concerns over stagflation risks.

Federal Reserve Faces a Stagflation Challenge

The OECD flagged a difficult backdrop for policymakers: slowing growth paired with stubbornly high inflation, projected to reach 3.2% in 2025 and possibly touch 4% by year-end. This forces the Fed into a corner. Rate cuts could be delayed or muted, as higher inflation expectations may keep interest rates elevated to anchor price stability, even if it suppresses output. Persistent tariff changes and legal uncertainty further complicate the Fed’s decision-making, pushing it toward more reactive, data-driven strategies instead of clear forward guidance.

Treasury Market Volatility: Yield Curve Set to Flatten Further?

Fixed income traders face opposing forces. Slower growth typically leads to lower long-term yields, but inflation pressure and the likelihood of prolonged Fed tightening could buoy short-term yields. Two-year Treasuries may remain elevated, while long-end yields are capped by recession fears, flattening the yield curve. This inversion scenario highlights investor doubts about long-term growth while acknowledging inflation remains a policy priority.

U.S. Dollar Strength Backed by Rate Premium and Productivity Edge

Despite softer GDP expectations, the dollar remains supported by its rate advantage and safe-haven status. The OECD emphasized strong U.S. productivity gains, particularly from AI and tech, which could make the U.S. outperform global peers. Tariff-related cost hikes might reduce imports and narrow the trade deficit—further underpinning the greenback. But a too-strong dollar could eventually bite back by making U.S. exports less competitive.

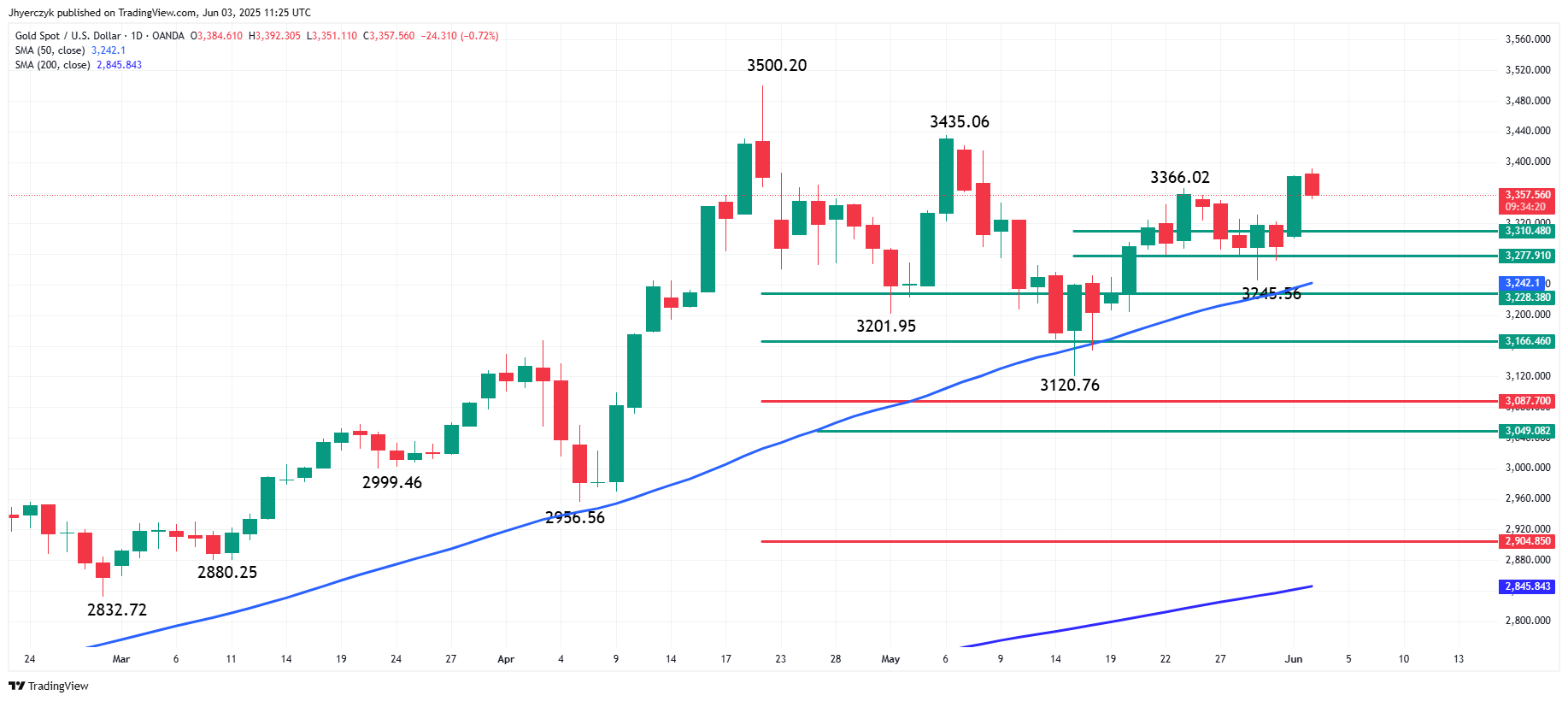

Gold Gathers Momentum on Inflation and Policy Uncertainty

Gold is positioned to benefit from this unique mix of elevated inflation, slower growth, and geopolitical uncertainty. As real rates potentially fall into negative territory, the opportunity cost of holding gold diminishes. The OECD’s reference to “unprecedented” policy and trade uncertainty may also spark fresh central bank demand and safe-haven flows, giving bullion additional support.

Equity Market Outlook: Sector Rotation and Defensive Plays Likely

Equities could face valuation pressure as higher rates reduce future earnings appeal. Growth stocks are most at risk, while tech and productivity-centric sectors may hold up better. Energy and materials could see upside on inflation, while consumer discretionary and multinationals face margin risk from tariffs and soft demand. Domestic-facing firms may outperform under a potential “America First” investor bias.

Market Forecast: Cautious Tilt Across Assets

Short-term outlook favors a hawkish Fed, flatter Treasury curve, firm dollar, and bullish gold bias. Equities may see defensive rotation and heightened volatility as markets digest the stagflation narrative and await clearer Fed signals. Traders should brace for sustained uncertainty with selective sector exposure.

More Information in our Economic Calendar.

About the Author

James HyerczykProfits & Punchlines

Mr.Hyerczyk is a technical analyst, market researcher, educator and trader. Jim is an expert in the area of patterns, price and time analysis, Forex and stocks.

Advertisement