Advertisement

Advertisement

Hang Seng Index Dips As Tariff Risks Overshadow Stimulus Pledges – Weekly Recap

By:

Key Points:

- Nasdaq drops for a third week as trade war fears escalate, sending gold to $3k.

- Beijing pledges stimulus to counter trade war threats, boosting investor sentiment.

- Nikkei edges higher as a weaker Yen lifts Japanese stock market outlook.

US Markets: Nasdaq Extends Losing Streak to Four Weeks

US equity markets posted losses in the week ending March 14 amid rising tariff tensions and recession fears. Sweeping US tariffs fueled concerns about higher import prices, inflation, and a more hawkish Fed. Higher prices and inflation may curb private consumption, which contributes over 60% to GDP.

The US rolled out sweeping 25% US tariffs on aluminum and steel, prompting China to threaten retaliatory measures. Meanwhile, the EU imposed 50% tariffs on US whiskey, while President Trump escalated tensions, warning of 200% tariffs on EU wines and spirits. These developments heightened fears of a global trade war, further unsettling markets.

The Nasdaq Composite Index and the S&P 500 extended their losing streaks to four weeks, posting losses of 2.43% and 2.27%, respectively. The Dow fared worse, falling 3.07% in the week.

US Economic Indicators: Inflation and Labor Market Cool

US labor market and inflation data fueled hopes for a Fed rate cut in June, which could open the door to additional rate cuts in H2 2025. Lower interest rates reduce borrowing costs, potentially improving corporate profits and demand for risk assets.

Key stats from the week included:

- US CPI Report: Annual inflation rate fell from 3% in January to 2.8% in February, while core inflation eased to 3.1%, down from 3.3% in January.

- Producer Prices: As a leading inflation indicator, producer prices rose 3.2% year-on-year in February, down from 3.7% in January, signaling a softer inflation outlook.

- US Jobless Claims: The jobless claims 4-week average rose to 226k (week ending March 8), up from 224.5k (week ending March 1). A weaker labor market could lower wages and reduce consumer spending, easing inflationary pressures.

Despite weaker labor market data, concerns over tariff-induced inflation tempered expectations for a June Fed rate cut. According to the CME FedWatch Tool, the probability of the Fed lowering rates in June fell from 81.7% (March 7) to 77.1% (March 14).

China’s Economic Stimulus Measures Bolster Investor Confidence

China ramped up efforts to stabilize its economy as trade tensions with the US escalated. On March 13, The People’s Bank of China (PBoC) pledged policy measures, boosting market optimism. Pledges included:

- Interest rate and Reserve Requirement Ratio (RRR) cuts when required.

- Incorporate new policy tools to foster tech innovation, consumption, and trade.

- Reduce social financing costs.

- Deliver liquidity to bolster economic growth.

The PBoC’s announcement followed the third session of the 14th National People’s Congress (NPC), where lawmakers announced a 2025 growth target of around 5%.

Hang Seng Index and Mainland China Markets Diverge on Trade and Stimulus News

The Hang Seng Index fell 1.12% in the week ending March 14, partially reversing the previous week’s 5.62% gain. Investors locked in profits amid fears of a full-blown US-China trade war. However, the PBoC’s policy pledges lifted sentiment and boosted demand for Hong Kong-listed stocks on March 14.

The Hang Seng Mainland Properties Index dropped 1.88% in the week, while the Hang Seng Technologies Index lost 2.59%. Alibaba (09988.HK) fell 3%, with Tencent (80700.HK) declining by 2.01%. Baidu (09888.HK) bucked the trend, advancing 0.94% after announcing a new partnership with Tesla (TSLA) to enhance self-driving technology in China.

Meanwhile, China’s ongoing policy pledges and a potential US-China economic divergence boosted demand for Mainland-listed stocks. The CSI 300 and Shanghai Composite Index extended gains from the previous week, rising 1.59% and 1.39%, respectively.

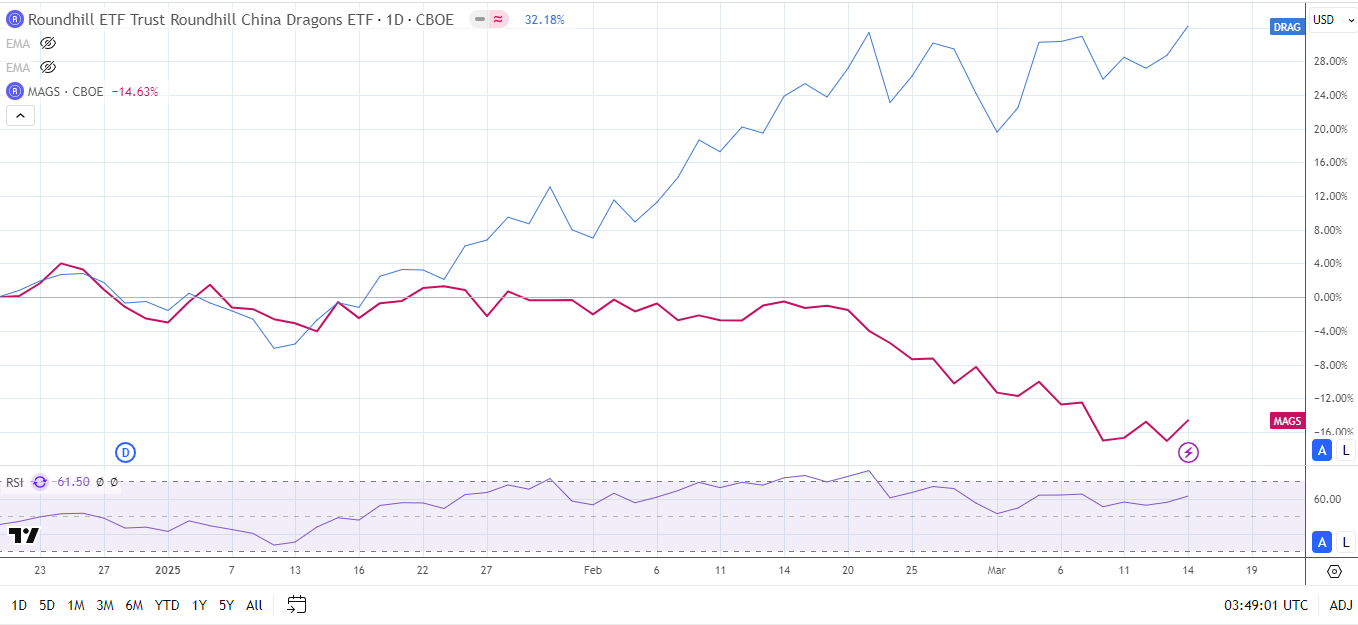

Brian Tycangco, editor and analyst at Stansberry Research, shared a chart showing China and US Tech sector trends, commenting:

“Looks like the long China tech, short US tech trade is still firmly in play.”

For more analysis on the Hang Seng Index and global market trends, click here.

Commodities: Gold Hits $3K as Iron Ore and Crude Oil Hold Steady

Commodity markets delivered a mixed performance amid trade tensions and shifting supply-demand dynamics.

- Gold rallied 2.55% in the week ending March 14, striking a record high of $3,005 before easing back to close the week at $2,984. Fears of a tariff-induced US recession boosted demand for safe-haven assets.

- Iron ore prices dipped 0.16% to $759 as investors considered the impact of steel tariffs on demand.

- Crude oil edged 0.03% higher to $67.23 as falling gasoline inventories and softer-than-expected crude inventories supported current price levels.

ASX 200 Extends Losing Streak to Four Weeks

The ASX 200 declined by 1.99% in the week ending March 14, marking its fourth consecutive weekly loss.

US steel and aluminum tariffs and potential full-blown US trade wars with the EU and China impacted risk assets. News that Australia would not receive exemptions from US aluminum and steel tariffs added to the negative sentiment.

The Nasdaq’s continued retreat weighed on tech stocks, while tariff and US recession concerns weighed on banking stocks.

- The S&P/ASX All Technology Index tumbled 4.95%.

- Banking Sector: The Commonwealth Bank of Australia (CBA) slid by 4.13%, while Westpac Banking Corp (WBC) dropped 3.14%.

- Gold Stocks: Meanwhile, Northern Star Resources (NST) jumped 3.77% on the upswing in gold prices.

Nikkei Index Edges Higher on Yen Weakness

A weaker Japanese Yen bolstered demand for Japanese stocks as the USD/JPY rose 0.40% to close the week at 148.618. A softer Yen boosts Japanese corporate earnings by making exports more competitive.

- Tokyo Electron (8035) gained 1.73% in the week ending March 14, while Softbank Group (9984) fell 1.47% amid the US tech sector sell-off

- Bank stocks led the gains on expectations of a more hawkish BoJ rate path. Mitsubishi UFJ Financial Group rallied 4.06%, with Sumitomo Mitsui Financial Group rising 3.01%.

Market Outlook: Key Events to Watch

The upcoming week will be crucial for the Asian markets. Economic data, central bank maneuvers, and tariff developments will be focal points. Key events include:

- US Tariffs: Trump’s shifting stance remains a key risk factor for global markets. Any further policy shifts will influence investor sentiment.

- China Stats and Beijing Stimulus: Crucial economic data from China could influence stimulus expectations and risk sentiment on March 17. Stimulus measures to boost domestic consumption could further mitigate tariff risks, supporting demand for HK and Mainland-listed stocks.

- US Federal Reserve and Bank of Japan Interest Rate Decisions: The Fed and the BoJ will announce interest rate decisions and provide forward guidance this week. Monetary policy divergence could impact the USD/JPY, potentially raising the threat of a Yen carry trade unwind.

With economic uncertainty and market volatility persisting, traders should closely monitor global macroeconomic trends and policy shifts here to navigate risks effectively.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Did you find this article useful?

Latest news and analysis

Advertisement