Advertisement

Advertisement

Hang Seng Index Falls as Trump Leads – Swing States Up for Grabs

By:

Key Points:

- Hang Seng Index drops 1.86% as Trump's tariff threats loom, impacting real estate and tech giants like Alibaba.

- Nikkei jumps 2.26% as USD/JPY hits 154, fueled by Trump's potential win, boosting export-driven stocks.

- ASX 200 rises 0.84%, led by banking and mining stocks, but iron ore faces pressure from Trump's tariff worries.

In this article:

US Markets: Trump Bets Boost Risk Sentiment

As Trump takes an early lead in the presidential race, global markets are reacting in real-time. Can a Trump victory reshape economic outlooks worldwide?

On Tuesday, November 5, US equity markets rallied as investors reacted to Trump’s early lead in the US presidential election. The Nasdaq Composite Index advanced by 1.43%, with the Dow and the S&P 500 gaining 1.02% and 1.23%, respectively.

US Services PMI Signal Robust US Economy

On Tuesday, the all-important ISM Services PMI unexpectedly increased from 54.9 in September to 56.0 in October. Economists had expected the PMI to drop to 53.8. Accounting for around 80% of the US economy, the service sector numbers removed immediate fears of a soft US economic landing.

The sharp increase in the Employment Index within the PMI report reduced expectations of a December Fed rate cut. According to the CME FedWatch Tool, the probability of a 25-basis point Fed rate cut to 4.25% fell from 79.6% on November 4 to 64.8% on November 5.

Despite bets on a more hawkish Fed rate path, risk sentiment remained positive, supported by Trump’s early lead.

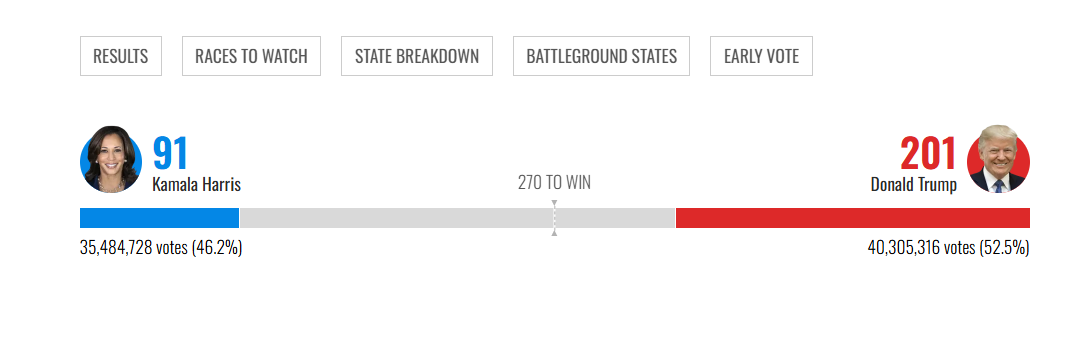

US Presidential Election: Trump Takes a Big Lead

On Wednesday, November 6, Trump led Kamala Harris with 201 to 91 electoral votes, driving demand for the US dollar. 10-year US Treasury yields surged 3.60% as investors priced in a Trump win. Trump needs 277 electoral votes to win, with swing states still up for grabs.

Standing Committee National People’s Congress in Focus

On Wednesday, Standing Committee National People’s Congress-related news requires consideration. Reaction to the US presidential election and stimulus measures to drive consumer spending and counter a potential US trade war could influence risk sentiment.

Hang Seng and Mainland China Equities Struggle on US Election Results

In Asian markets, the Hang Seng Index declined by 1.86% on Wednesday morning. Results from the US presidential election fueled fears of a Trump win. Trump warned of 60% tariffs on Chinese goods, potentially impacting the Chinese economy.

Real estate and tech stocks stumbled in the morning session. The Hang Seng Mainland Properties Index and the Hang Seng Tech Index slid by 1.71% and 1.96 %, respectively. Tech giants Alibaba (9988) and Baidu (9888) saw losses of 2.59% and 1.55%, respectively. JD.com (9618) slumped by 5.80%.

Mainland China’s equity markets gave up early gains, with the CSI 300 and the Shanghai Composite falling 0.47% and 0.27%, respectively. Fears of a Trump victory overshadowed hopes for stimulus measures from Beijing to boost consumer demand.

Nikkei Surges as USD/JPY Jumps on Trump Bets

In Japan, the Nikkei Index surged by 2.26% on Wednesday morning. Expectations for a Trump victory in the presidential election drove the USD/JPY to 154, fueling demand for Nikkei Index-listed stocks.

Softbank Group (9984) and Tokyo Electron (8035) rallied 2.79% and 2.49%, respectively. Export stocks Sony Corp. (6758) and Nissan Motor Corp. (7201) advanced by 2.13% and 1.44%, respectively.

ASX 200 Tracks US Futures Higher

The ASX 200 Index advanced by 0.84% on Wednesday morning, tracking the US futures markets higher. Gains were broad-based, with banking, gold, mining, oil, and tech stocks contributing to the gains. The S&P/ASX All Technology Index was up 1.41% in the morning session.

Banking stocks National Australia Bank gained 1.11%, with Commonwealth Bank of Australia advancing by 0.84%.

Mining giants Rio Tinto Ltd. (RIO) and BHP Group Ltd. (BHP) were up by 0.72% and 0.42%, respectively. Iron ore spot prices advanced overnight, supporting the morning gains. However, iron ore spot prices were down on Wednesday, as a Trump win could impact China’s demand for iron ore through tariffs. Mining stocks may give up early gains if Trump extends his lead.

Looking Ahead

Looking ahead, investors should monitor the US Presidential Election. The focus will be on the swing states. A Trump victory would continue driving US dollar demand and pressure HK and Mainland China-listed equities. Conversely, a Harris victory could reverse the morning trends.

National People’s Congress Standing Committee (NPCSC) meeting-related news also requires consideration. Beijing’s response to the US election and fresh stimulus could influence risk sentiment. Stay informed with our latest news and analysis to manage your risks effectively.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement