Advertisement

Advertisement

Japanese Yen and Aussie Dollar News: BoJ vs. Fed Rate Path Battle Heats Up

By:

Key Points:

- Japan’s jobless rate drops to 2.4%, boosting BoJ rate hike bets and increasing pressure on the USD/JPY exchange rate.

- Weak Australian producer prices heighten RBA rate cut expectations, pushing AUD/USD lower amid US inflation concerns.

- US Core PCE inflation expected at 2.8% YoY, influencing Fed rate cut bets and driving near-term USD/JPY and AUD/USD price trends.

Japan’s Unemployment and Retail Sales Boost BoJ Rate Hike Expectations

On Friday, January 31, Japan’s economic data influenced the USD/JPY pair’s trajectory and sentiment toward the Bank of Japan’s rate path.

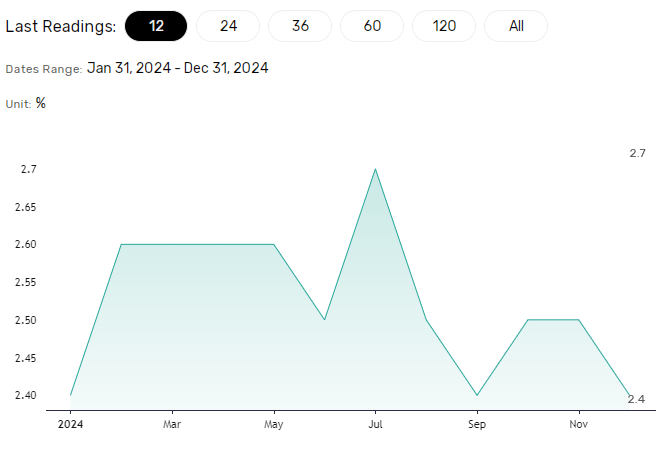

Japan’s unemployment rate fell to 2.4% in December, down from 2.5% in November, signaling a resilient labor market. Tighter labor market conditions could support wage growth, fueling consumer spending and demand-driven inflation.

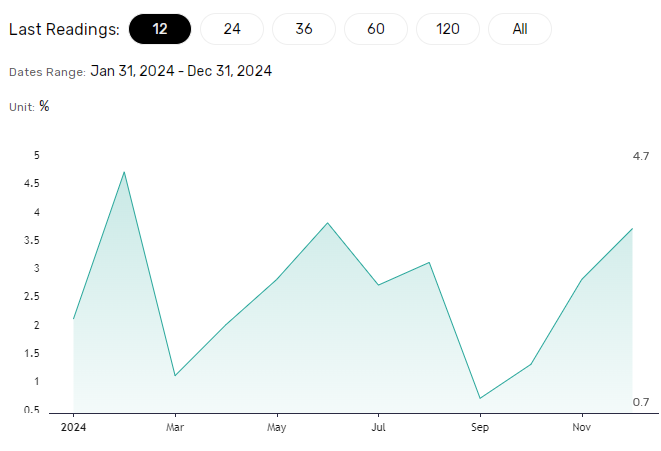

Retail sales also pointed to rising inflationary pressures, climbing 3.7% year-on-year in December, up from 2.8% in November.

The lower unemployment rate and jump in consumer spending could raise expectations of another BoJ rate hike in H1 2025. December’s data was significant as the BoJ has highlighted a willingness to tighten monetary policy further if economic indicators support the move.

On January 30, BoJ Deputy Governor Himino reinforced Governor Kazuo Ueda’s stance, stating that further policy moves hinge on economic and price developments. He added that the BoJ will raise rates if the economy and prices align with forecasts.

A more hawkish BoJ rate path would pressure the USD/JPY pair, potentially pulling it toward the 153 level.

USD/JPY Trends: US Inflation in Focus

Shifting to the US, the Personal Income and Outlays report could dictate the near-term Fed rate path. Economists expect the Core PCE Price Index to rise 2.8% year-on-year in January, mirroring December’s increase.

Higher inflation could dampen expectations for an H1 2025 Fed rate cut, supporting a USD/JPY move toward the 50-day Exponential Moving Average (EMA). A break above the 50-day EMA would bring the 156.884 resistance level into play.

Conversely, a softer reading may revive bets on a near-term Fed rate cut, potentially dragging the USD/JPY pair toward 153.

Beyond inflation, personal income and spending will also be crucial. Rising trends in income and spending could indicate upward pressure on consumer prices. This scenario would support Fed Chair Powell’s call for caution regarding inflation and further monetary policy easing.

For a comprehensive analysis of USD/JPY trends and trade data insights, check out our detailed reports here.

The AUD/USD: Producer Prices Boost RBA Rate Cut Expectations

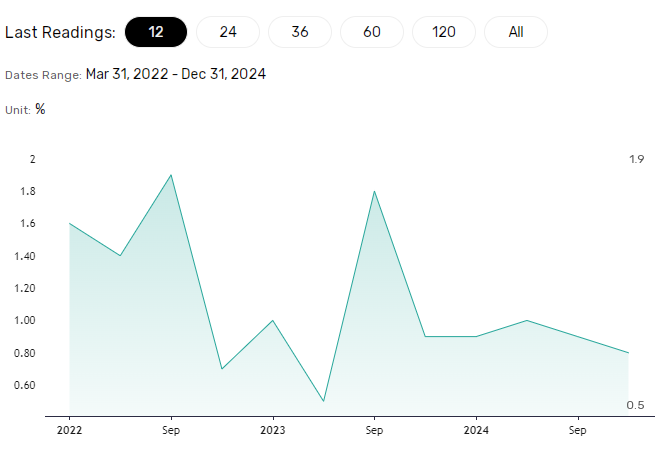

For the Australian dollar, Aussie producer prices pressured the AUD/USD pair. Producer prices rose 0.8% quarter-on-quarter in Q4 2024 after increasing by 1.0% in Q3 2024. The Q4 numbers suggest softer inflationary pressures as producers lower prices in a weakening demand environment, passing cost savings on to consumers.

Expectations of a further softening in inflationary pressures could bolster bets on multiple H1 2025 RBA rate cuts. The AUD/USD pair dropped from $0.62111 to $0.62048 in response to the softer reading, reflecting investor sentiment toward the RBA rate path.

In December, RBA Governor Michele Bullock discussed the importance of inflation trends, stating:

“If inflation continues to soften, the RBA could become confident about cutting interest rates. […] The RBA will look at the data ahead of the February meeting, including monthly inflation and labor market data.”

For a comprehensive analysis of AUD/USD trends and trade data insights, visit our detailed reports here.

Australian Dollar Daily Chart

Turning to the US session, the Personal Income and Outlays Report could influence the US-Aussie interest rate differential. Hotter-than-expected inflation and personal income/spending could sink Fed rate cut bets, widening the interest rate differential in favor of the US dollar. In this scenario, the AUD/USD pair may drop toward the upper band of its descending channel.

Conversely, softer inflation and a drop in income and spending could retrigger Fed rate cut bets. A more dovish Fed stance may push the AUD/USD pair toward the 50-day EMA. A break above the 50-day EMA could enable the bulls to target the $0.63623 resistance level.

Market Trends: Central Banks Drive Sentiment

Central banks remain key drivers of currency markets. The BoJ’s forward guidance could increase USD/JPY’s sensitivity to Japanese economic data, while US data will influence broader dollar trends. Meanwhile, AUD/USD movements will hinge on expectations surrounding the RBA’s policy stance.

Additionally, global factors such as US trade policies and China’s stimulus measures will likely influence broader market sentiment in the coming weeks.

Click here for live updates and trading strategies!

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement