Advertisement

Advertisement

Microsoft Set for Continued Bullish Momentum in 2024

By:

Key Points:

- Microsoft Corporation reported strong financial results for Q3 FY24, with significant revenue and income growth driven by its cloud business and AI solutions.

- Microsoft's cloud revenue experienced substantial growth, attributed to significant Azure contracts and strong execution in core sales areas.

- Positive performance across Microsoft's key business segments suggests a bullish outlook.

- The technical performance of Microsoft is strongly bullish and suggests a continued rally in 2024.

In this article:

The company achieved significant revenue growth, substantially increasing operating income and net income. Diluted earnings per share (EPS) also increased significantly. These impressive results were primarily driven by the thriving cloud business and the successful implementation of AI solutions through its Copilot and Copilot stack.

Additionally, Microsoft Cloud revenue experienced substantial growth, attributed to significant Azure contracts and strong execution in core sales areas. The company’s financial health is further highlighted by its commercial development, with significant booking increases and the commercial remaining performance obligation. Microsoft’s commitment to shareholder returns, operational efficiency, and strategic investments in cloud and AI infrastructure underscores its promising outlook, positioning it favourably for sustained growth and market dominance.

This article examines Microsoft stock’s fundamental and technical performance to analyze market dynamics and identify investment opportunities for long-term investors. It is observed that the stock price is currently trading at record highs and is expected to continue bullish momentum in the coming months.

Financial Highlights

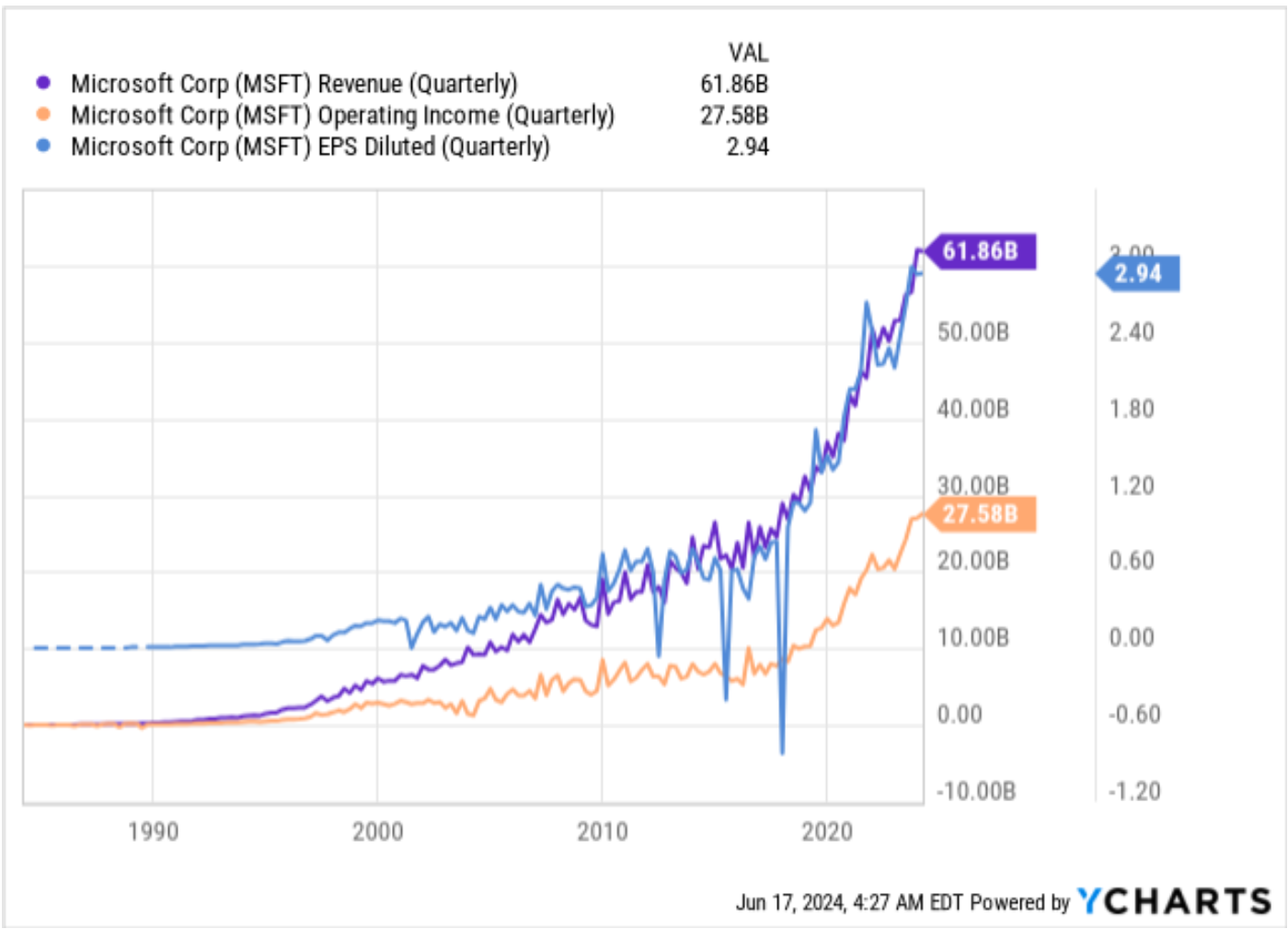

Microsoft revenue reached $61.86 billion in Q3 FY24 earnings report, marking a 17% increase compared to Q3 FY23. Operating income was also strong at $27.58 billion, up 23%, while net income grew by 20% to $21.9 billion. Additionally, diluted EPS stood at $2.94, showing a 20% year-over-year increase. The chart below shows a parabolic increase in these metrics, indicating the company’s potential for future profitability. These impressive results were driven by Microsoft’s strong cloud business and the successful implementation of AI solutions through its Copilot and Copilot stack.

The quarterly commercial highlights further strengthen Microsoft’s financial health. Notably, Microsoft Cloud revenue for Q3 FY24 was $35.1 billion, an increase of 23% from Q3 FY23. This growth is attributed to large, long-term Azure contracts and effective execution across the company’s core sales motions.

The commercial business also saw significant growth, with commercial bookings rising by 29% year-over-year and the commercial remaining performance obligation increasing to $235 billion, up 20%. On the other hand, Microsoft Cloud’s gross margin percentage slightly decreased to 72% due to higher scaling costs for AI infrastructure.

The financial highlights indicate a solid commitment to shareholder returns and operational efficiency. Microsoft returned $8.4 billion to shareholders through dividends and share repurchases. Operating expenses were $15.8 billion, a 10% increase driven by the acquisition of Activision. The effective tax rate was 18%, and capital expenditures amounted to $14.0 billion, supporting demand in cloud and AI offerings.

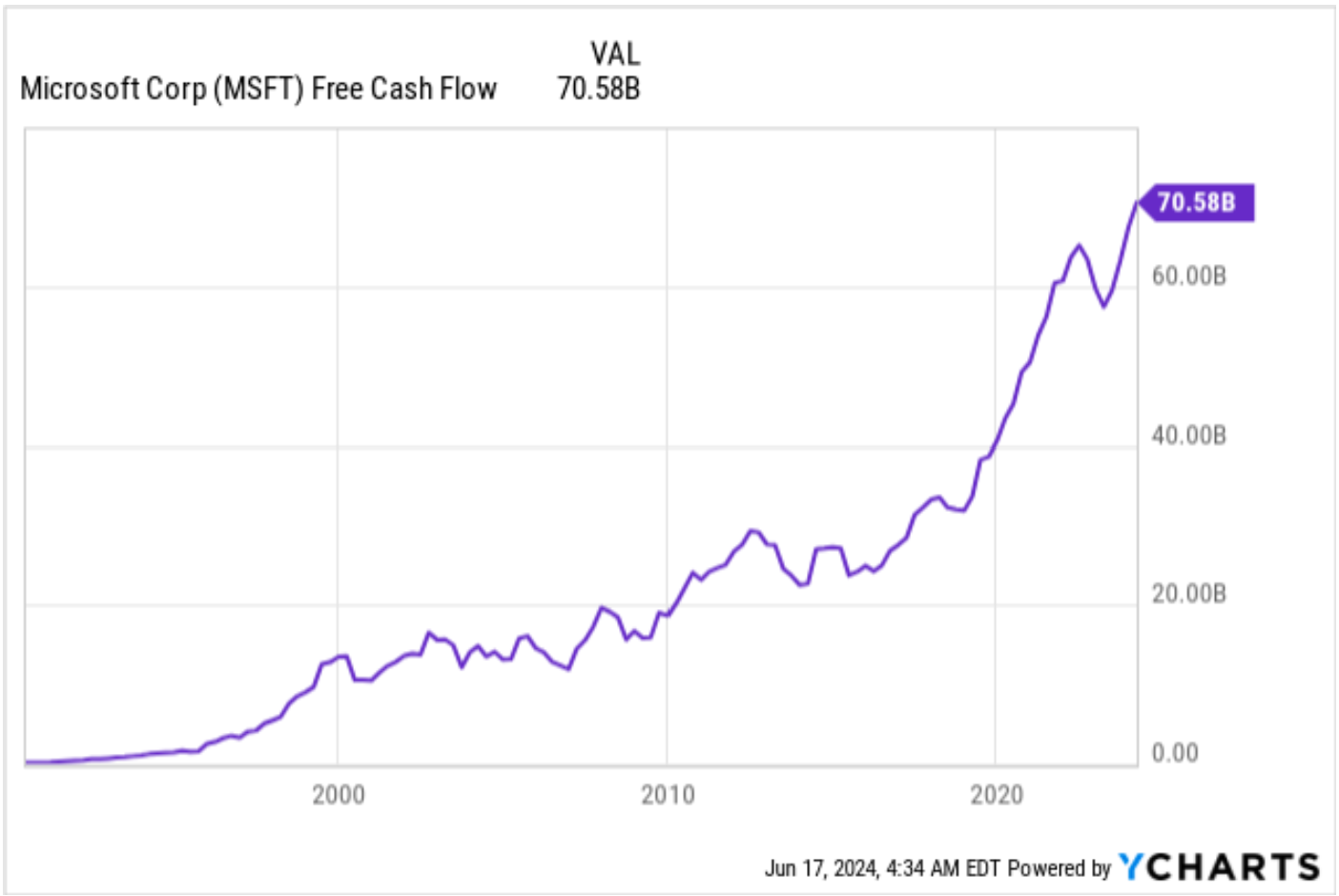

Free cash flow shows a strong trend with $70.58 billion, as shown in the chart below. These positive financial metrics are likely to favour Microsoft’s stock price, as they reflect strong business fundamentals and growth prospects in the cloud and AI sectors. Investors may respond positively, driving up the stock price due to the demonstrated financial strength and future potential highlighted in the earnings report.

Business Segments and Future Projections

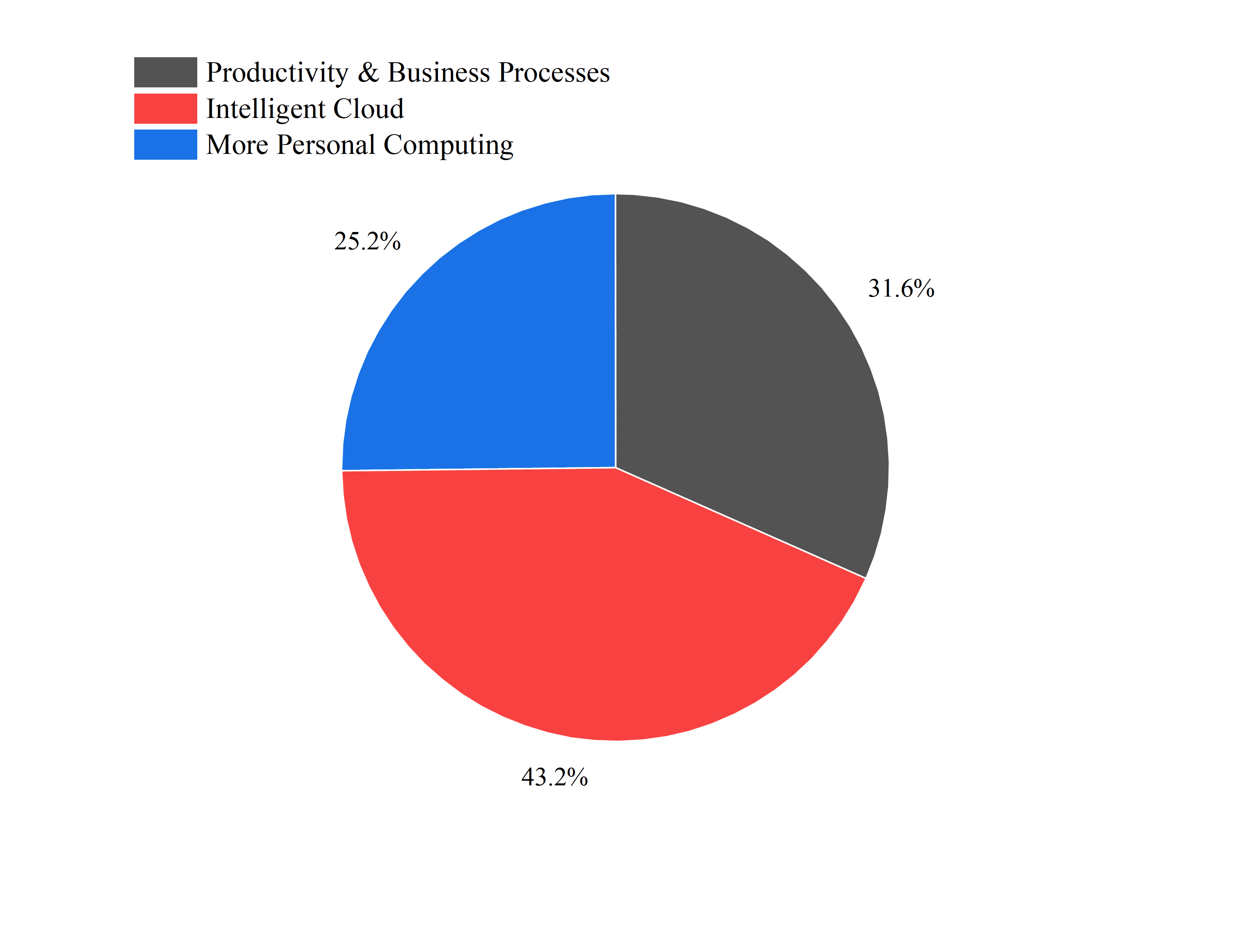

Microsoft’s financial performance in Q3 FY24 demonstrates significant growth across its primary business segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The chart below shows that the highest percentage of revenue in Q3 FY24 was contributed by the Intelligent Cloud segment, accounting for 43.2% of overall revenue, indicating strong performance in this segment.

The Productivity and Business Processes segment contributed 31.6% of revenue, while the More Personal Computing segment contributed 25.2%. Revenue distribution indicates that all segments are performing well, showcasing the company’s strength.

In the Productivity and Business Processes segment, revenue grew 13% year-over-year, driven by solid performances in Office Commercial products and cloud services, which increased by 13%, and Dynamics products and cloud services, which saw a 19% increase. LinkedIn revenue also grew by 10%, reflecting Microsoft’s continued success in business networking and professional growth solutions.

The Intelligent Cloud segment showcased substantial growth, with revenue rising 24% year-over-year. This growth was primarily driven by Azure and other cloud services, which saw a 31% increase, highlighting the strong demand for Microsoft’s cloud computing solutions.

Server products and cloud services revenue also grew by 24%, demonstrating the robust performance of Microsoft’s data centre and enterprise solutions. The segment’s gross margin dollars grew by 20%, and operating income surged by 32%, highlighting the profitability of Microsoft’s cloud offerings.

In the More Personal Computing segment, revenue increased by 17%, with notable growth in Windows OEM revenue (up 11%) and Windows Commercial products and cloud services revenue (up 13%). The acquisition of Activision significantly boosted gaming revenue, with Xbox content and services revenue increasing by 62%. However, device revenue declined by 17%, indicating a shift towards higher-margin premium products. The search and news advertising revenue grew by 12%, driven by higher search volume, contributing to the overall revenue growth in this segment.

The positive performance across these segments indicates a bullish outlook for Microsoft. The significant growth in cloud services and enterprise solutions positions Microsoft favourably in the rapidly expanding cloud market. The strong performance in the Productivity and Business Processes segment highlights the company’s ability to provide essential tools for businesses and professionals. Additionally, the substantial increase in gaming revenue following the Activision acquisition demonstrates Microsoft’s strategic expansion into the gaming industry.

These factors will likely positively impact Microsoft’s stock price as investors recognize the company’s strong market position and growth potential in key technology sectors. The robust financial performance and strategic investments in high-growth areas will likely drive investor confidence and increase Microsoft’s stock value.

Based on the solid performance, the company expects substantial revenue in Q4 FY24 and for 2024. The Productivity and Business Processes segment is expected to generate between $19.9 billion and $20.2 billion. The Intelligent Cloud segment anticipates revenues between $28.4 billion and $28.7 billion, driven by strong demand for Azure and other cloud services. The More Personal Computing segment is forecasted to bring in $15.2 billion to $15.6 billion, with growth in Windows OEM revenue and Xbox content and services offsetting a decline in device revenue.

Overall, the cost of goods sold (COGS) and operating expenses are expected to include adjustments related to the Activision acquisition, with COGS ranging from $19.6 billion to $19.8 billion and operating expenses from $17.15 billion to $17.25 billion. Microsoft’s solid growth across its business segments suggests a positive outlook, likely supporting continued bullish momentum in its stock price.

Evaluation of Microsoft Technical Performance

Recap

Microsoft was expected to be bullish due to several compelling factors. The company’s consistent revenue growth over the past decade highlights its financial strength and market dominance, with significant contributions from cloud computing services. The acquisition of AI-powered services, including its partnership with OpenAI, positions Microsoft for a future competitive advantage in AI integration across its product suite. Furthermore, the expansion of the gaming industry, bolstered by the acquisition of Activision Blizzard, indicated substantial growth opportunities.

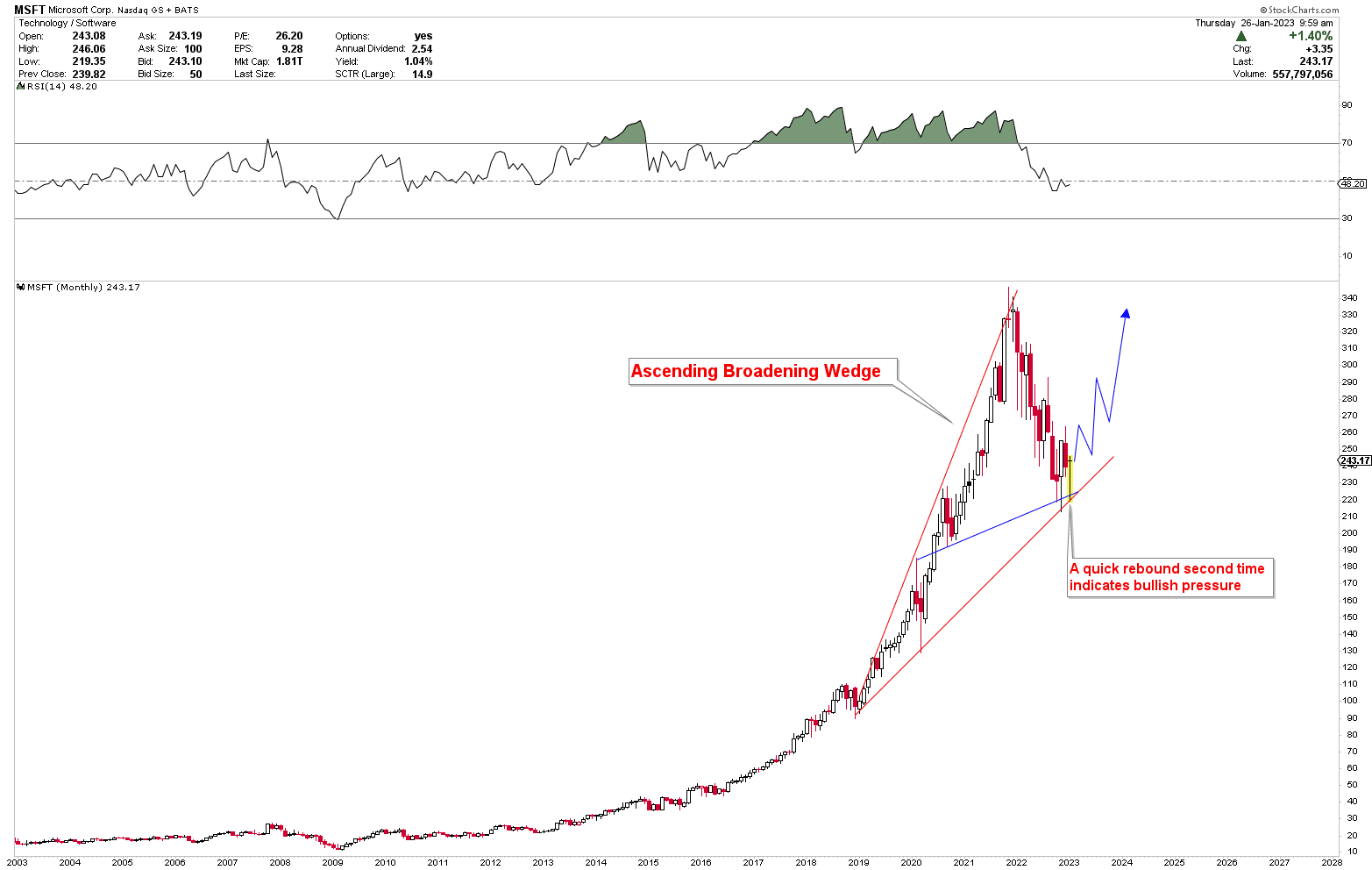

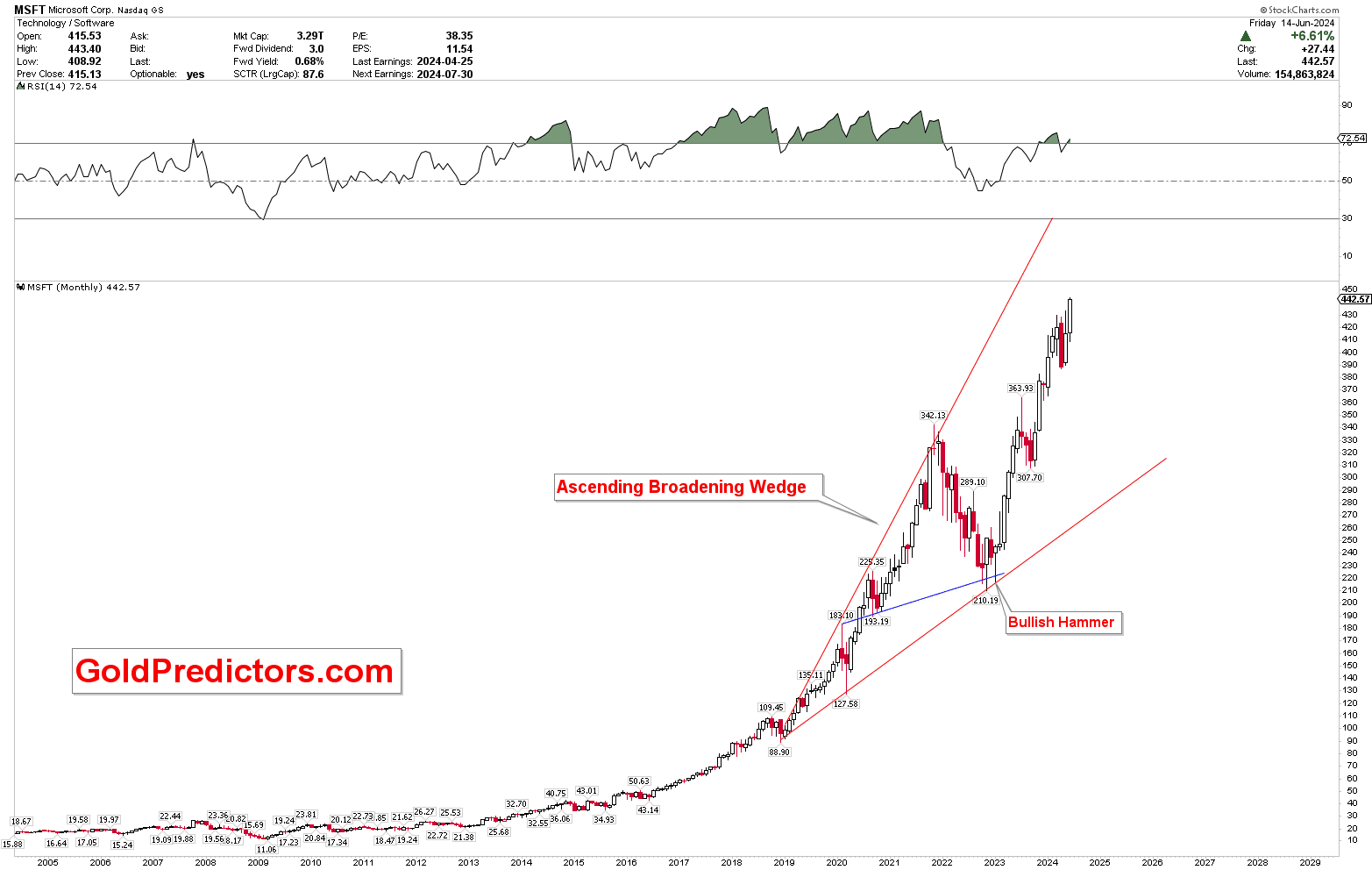

Technical analysis also supported a bullish outlook; the share price decline of 38.56% to a strong support level, combined with bullish chart patterns such as the ascending broadening wedge and double bottom formations, suggested a robust recovery and future price increases. These factors collectively underline Microsoft’s potential for sustained growth and strong performance in the coming years.

The Next Move in 2024

The stock price of Microsoft reacted as anticipated, hitting bottom at the strong support of the ascending broadening wedge pattern before surging to record highs, as shown in the chart below. The appearance of a bullish hammer at this support level underscored the price strength, resulting in a significant increase over the past few months. The chart below indicates that the price is still far from the target of this ascending broadening wedge, suggesting potential for future price growth.

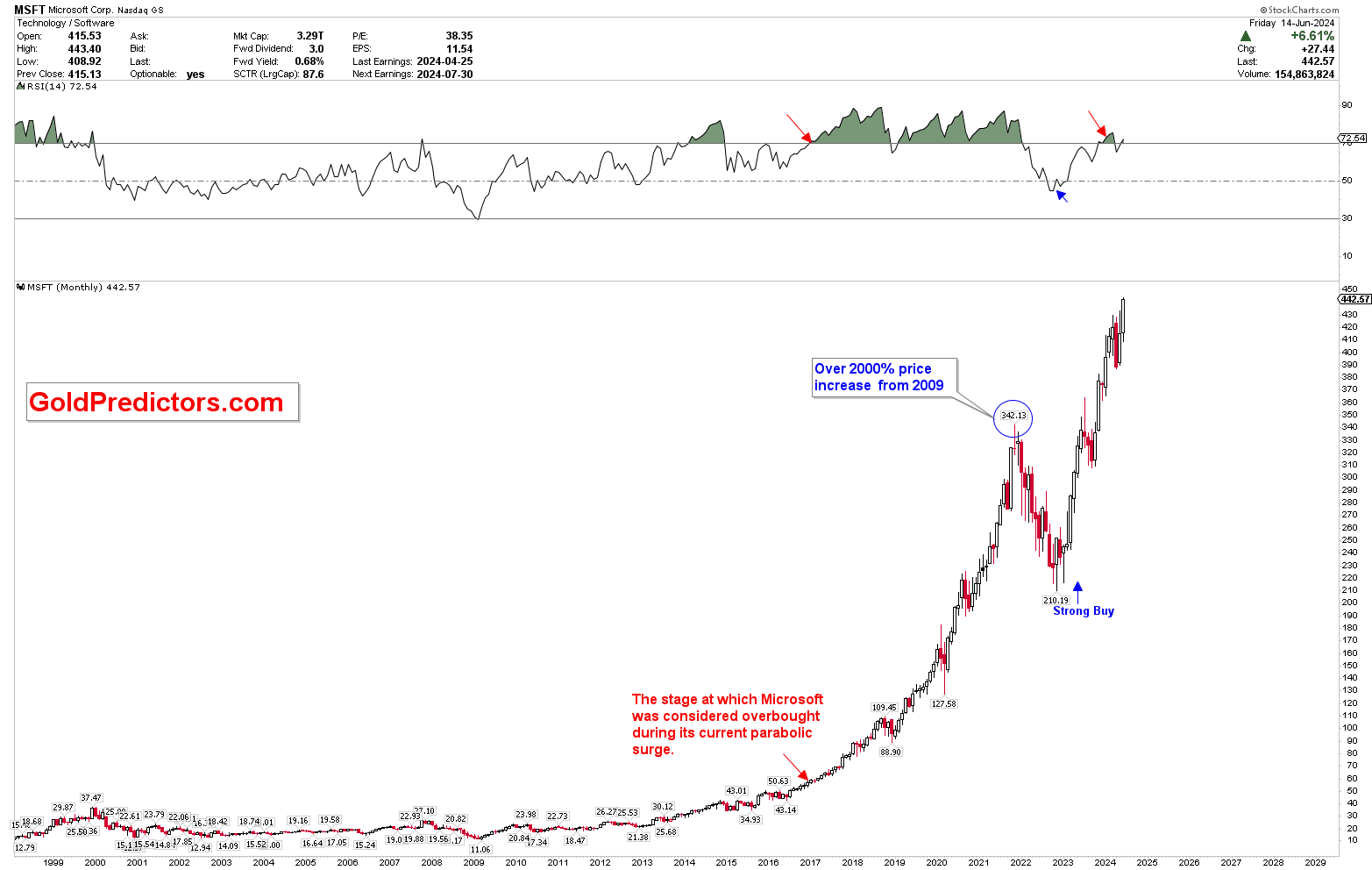

To further understand the above discussion, the monthly chart below shows the market’s overbought conditions, revealing that prices have continued to rise despite these conditions. The chart illustrates that Microsoft’s stock price became overbought in 2017, as indicated by the RSI indicator. Despite this overbought condition, the stock price increased by over 2000%, reaching record highs of $342.13.

The subsequent price correction from $342.13 found support at the mid-level of the RSI, signalling a strong buy opportunity confirmed by the ascending broadening wedge pattern. The chart also shows that Microsoft’s stock price is approaching the overbought region again, as indicated by the RSI. Still, it has strong potential for bullish momentum due to robust financial performance.

Price Targets & Investment Consideration

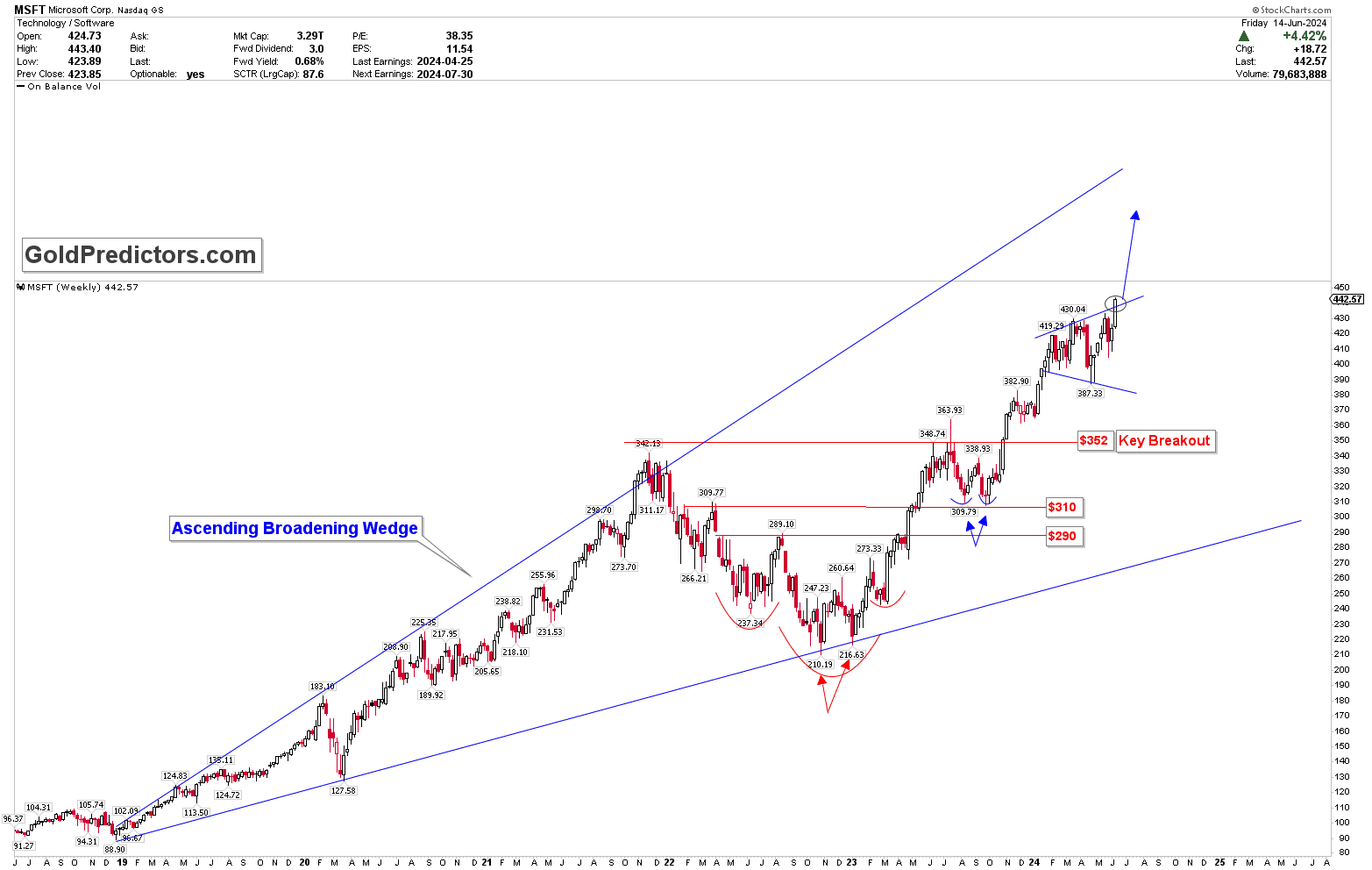

Since the monthly chart shows a solid long-term bullish technical picture for Microsoft, the medium-term outlook is also bullish, as seen on the weekly chart. This chart shows the same ascending broadening wedge in smaller time frames, indicating that the price has formed an inverted head and shoulders pattern, with the head at $210.19, shoulders around the $237 zone, and a neckline at $290-$310, with $352 as a key level.

The stock price broke the inverted head and shoulders pattern in 2023, initiating a strong surge in price. The perfect retest of $310 was a strong buy signal, leading prices to record highs above $400. This breakout keeps the bullish pattern active, and prices have formed a symmetrical broadening pattern at higher levels (highlighted by blue).

This pattern was broken last week when the price closed at $442.57, initiating the next surge to higher levels. The emergence of the symmetrical broadening pattern highlights intense volatility; however, the upside breakout suggests that this volatility may lead to a strong upward surge. The blue arrow shows the target of this ascending broadening wedge, which is above $500.

The chart indicates that the formation of the inverted head and shoulders pattern, followed by a double bottom and symmetrical broadening wedge, suggests a strongly bullish outlook and highlights the potential for continued bullish momentum in 2024. Therefore, investors can consider buying the stock during pullbacks to invest in the long-term rally. Since the price is trading at higher levels, buying on pullbacks is the right strategy for Microsoft investors.

Market Risks

One significant risk is the increasing competition in the cloud computing and AI sectors. Competitors such as Amazon Web Services (AWS) and Google Cloud are continuously innovating and expanding their services, which could potentially erode Microsoft‘s market share and pressure profit margins. Rapid technological advancements and the need for substantial investment in AI infrastructure pose challenges. If Microsoft fails to keep pace with these developments or its AI initiatives do not yield expected returns, the company could face competitive disadvantages.

Another risk is regulatory scrutiny and geopolitical tensions that could affect Microsoft’s global operations. The company’s substantial presence in international markets makes it vulnerable to changes in trade policies, tariffs, and regulatory requirements in different regions. For instance, ongoing tensions between the US and China could impact Microsoft’s supply chain and sales in these critical markets. Moreover, increasing regulatory focus on data privacy and security could lead to stringent compliance requirements and potential fines, affecting the company’s operations and profitability.

Economic factors and market conditions also present risks. Global economic downturns or recessions could reduce corporate IT spending, impacting demand for Microsoft’s products and services. These factors, combined with the inherent volatility of the technology sector, could result in stock price fluctuations and affect investor confidence.

From a technical perspective, the stock price has been trading at higher levels. Despite the continuation of the upward trend in 2024, it might be difficult for investors to enter at current levels as the market is overbought. Although prices are expected to continue rising, it will be tricky to enter the market due to the strong resistance.

Bottom Line

Microsoft Corporation’s strong financial performance in Q3 FY24 highlights its impressive growth and market potential. Driven by robust increases in revenue, operating income, net income, and EPS, the company demonstrates the effectiveness of its cloud business and AI solutions. The significant growth in Microsoft Cloud revenue and commercial bookings underscores the company’s financial health and strategic execution.

Additionally, the positive performance across its key business segments—Productivity and Business Processes, Intelligent Cloud, and More Personal Computing—indicates a bullish outlook for the future. Strategic investments in high-growth areas, such as cloud services, AI infrastructure, and the gaming industry, position Microsoft favorably for sustained market dominance and investor confidence.

As a result, Microsoft’s stock is poised for further appreciation, making it a compelling consideration for investors looking to capitalize on its long-term growth potential. The emergence of an inverted head and shoulders pattern, followed by a double bottom and a symmetrical broadening pattern, indicates that prices have set a bottom and are expected to continue bullish momentum in 2024.

Gold Predictors delivers trading signals for gold and silver. Please subscribe here to receive these trading signals.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Did you find this article useful?

Latest news and analysis

Advertisement