Advertisement

Advertisement

RBA Update: Central Bank Poised to Hold Cash Rate at 12-Year Peak

By:

The RBA will not likely adjust the OCR at tomorrow’s meeting and should maintain a moderately hawkish vibe.

In this article:

The Reserve Bank of Australia (RBA) will claim a portion of tomorrow’s limelight during Asia Pac hours at 4:30 am GMT as it announces its fourth update this year.

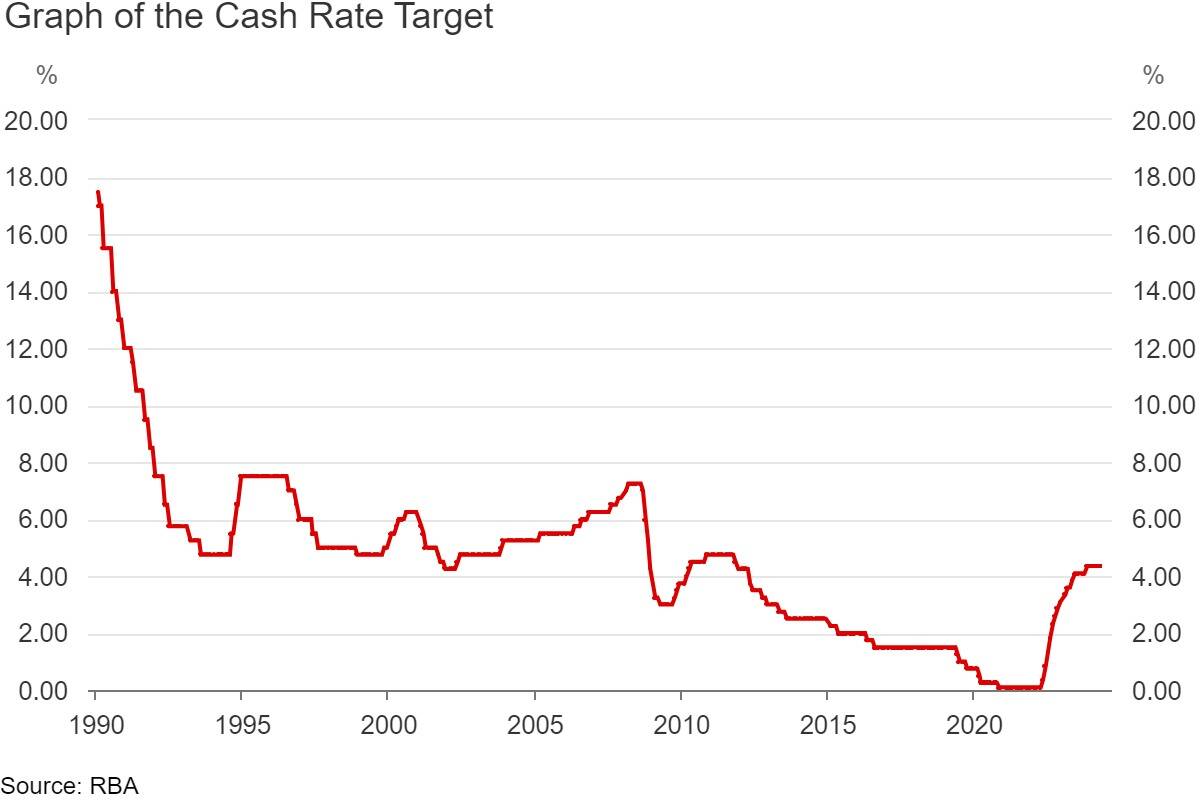

According to the OIS market, investors anticipate the central bank will leave the Official Cash Rate (OCR) at 4.35% (12-year high), marking the fifth consecutive meeting on hold. Investors also bet that the RBA remains on hold for the remainder of this year (17bps of easing priced in); the first 25bp rate cut is fully priced in for February’s meeting (-27bps). The rate announcement will accompany the rate statement and will be followed an hour later by the press conference held by RBA Governor Michelle Bullock.

The RBA’s update follows the European Central Bank (ECB) and the Bank of Canada (BoC) both cutting their overnight rates by 25bps and the FOMC holding the Fed funds target rate unchanged at 5.25%-5.50%, signalling a higher-for-longer narrative (the Summary of Economic Projections [SEP] showed Fed officials project one rate cut this year, down from three cuts forecast in the previous SEP).

Mixed Economic Picture Ahead of Rate Decision

The RBA is working with mixed signals regarding the economic landscape.

Inflation remains a thorn in the RBA’s side, having remained elevated this year. The central bank works with an inflation range between 2% and 3%, and the RBA forecasts we’ll venture into the upper edge of this range by December 2025 (+2.8%). According to the Monthly CPI Indicator, year-on-year inflation rose +3.4% in January and February to +3.5% in March and subsequently to +3.6% in April. Quarterly, inflation slowed to +3.6% in Q1 2024, down from +4.1% in Q4 2023.

The jobs market is tight and has helped push out rate-cut expectations. Employment change saw a back-to-back increase in total employment, adding nearly 40,000 new jobs to the economy in May, while the unemployment rate dipped back to 4.0% in May from April’s three-month peak of 4.1%.

On the growth front, it was pretty much flat in Q1 of this year; GDP rose +0.1% in Q1 and +1.1% year on year. In addition to softer economic activity, retail sales data came in soft, slowing to +0.1% in the month of April from March’s -0.4% fall (+0.2% consensus).

What Can We Expect?

The RBA will not likely adjust the OCR at tomorrow’s meeting and should maintain a moderately hawkish vibe. You may recall that previous guidance reiterated the point made at March and May’s meetings that the road back to the central bank’s inflation target is likely to be bumpy and that the Board ‘is not ruling anything in or out’.

It is doubtful that the central bank will stray too far away from its current bias and will repeat that future rate decisions will be dependent on incoming data. Consequently, void of any meaningful adjustment to the current bias, any reaction derived from the event will likely be short-lived.

DISCLAIMER:

The information contained in this material is intended for general advice only. It does not take into account your investment objectives, financial situation or particular needs. FP Markets has made every effort to ensure the accuracy of the information as at the date of publication. FP Markets does not give any warranty or representation as to the material. Examples included in this material are for illustrative purposes only. To the extent permitted by law, FP Markets and its employees shall not be liable for any loss or damage arising in any way (including by way of negligence) from or in connection with any information provided in or omitted from this material. Features of the FP Markets products including applicable fees and charges are outlined in the Product Disclosure Statements available from FP Markets website, www.fpmarkets.com and should be considered before deciding to deal in those products. Derivatives can be risky; losses can exceed your initial payment. FP Markets recommends that you seek independent advice. First Prudential Markets Pty Ltd trading as FP Markets ABN 16 112 600 281, Australian Financial Services License Number 286354.

About the Author

Aaron Hillcontributor

Aaron graduated from the Open University and pursued a career in teaching, though soon discovered a passion for trading, personal finance and writing.

Did you find this article useful?

Latest news and analysis

Advertisement