Advertisement

Advertisement

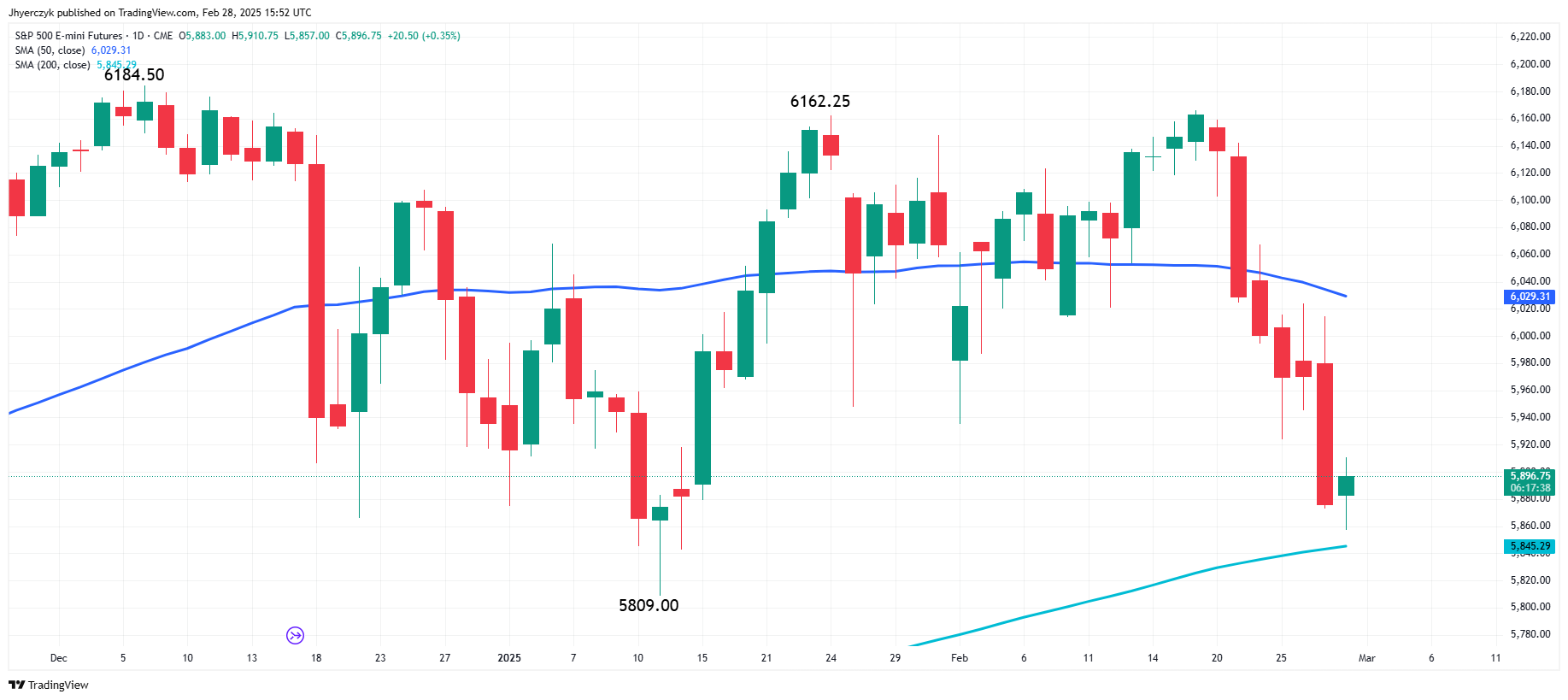

S&P 500 Edges Higher as Dell Falls 5.7%, Weekly and Monthly Losses Loom

By:

Key Points:

- S&P 500 gains Friday despite weak consumer spending data, with defensive sectors outperforming and tech stocks lagging.

- Stocks rise Friday as inflation holds steady; S&P 500 gains while Nvidia and NetApp lead tech sector declines.

- S&P 500 edges higher Friday despite economic slowdown fears, with consumer staples and utilities gaining 1%.

- Defensive sectors lift the S&P 500 Friday, offsetting tech struggles as Nvidia, Dell, and HP Inc. decline.

- Market rebounds Friday despite stagflation worries; traders focus on Fed Chair Powell’s upcoming commentary.

Wall Street Mixed as Consumer Spending Drop Fuels Economic Concerns

Wall Street’s main indexes traded mixed in a volatile session on Friday as weaker-than-expected consumer spending data in January raised concerns about a potential economic slowdown.

The Commerce Department reported a 0.2% decline in consumer spending, which makes up more than two-thirds of U.S. economic activity, following a 0.8% rise in December.

Inflation rose in line with expectations, but the spending dip added to worries that the U.S. economy might be stalling. Peter Cardillo, chief market economist at Spartan Capital Securities, noted the challenge for the Federal Reserve, stating, “If you add them together, that equals stagflation,” highlighting the difficult balance between curbing inflation and sustaining growth.

Will the Fed Stay Hawkish?

Traders closely monitored the data for clues on the Federal Reserve’s next policy moves. Despite signs of economic cooling, the Fed has maintained a hawkish stance, emphasizing the need to control inflation. Market data from LSEG indicated that traders expect the central bank to cut rates twice by December, a view that remained largely unchanged after the report.

Comments from Chicago Fed President Austan Goolsbee, expected later in the day, could provide additional insight into the Fed’s thinking. Investors are particularly wary of how the Fed will balance rate hikes with the risk of slowing economic growth under the new Trump administration’s trade policies, which could further stoke inflation.

Which Sectors Held Strong?

Defensive sectors outperformed, with consumer staples and utilities both climbing about 1%. These sectors often serve as safe havens during economic uncertainty. In contrast, technology stocks struggled to maintain gains, reflecting broader investor caution.

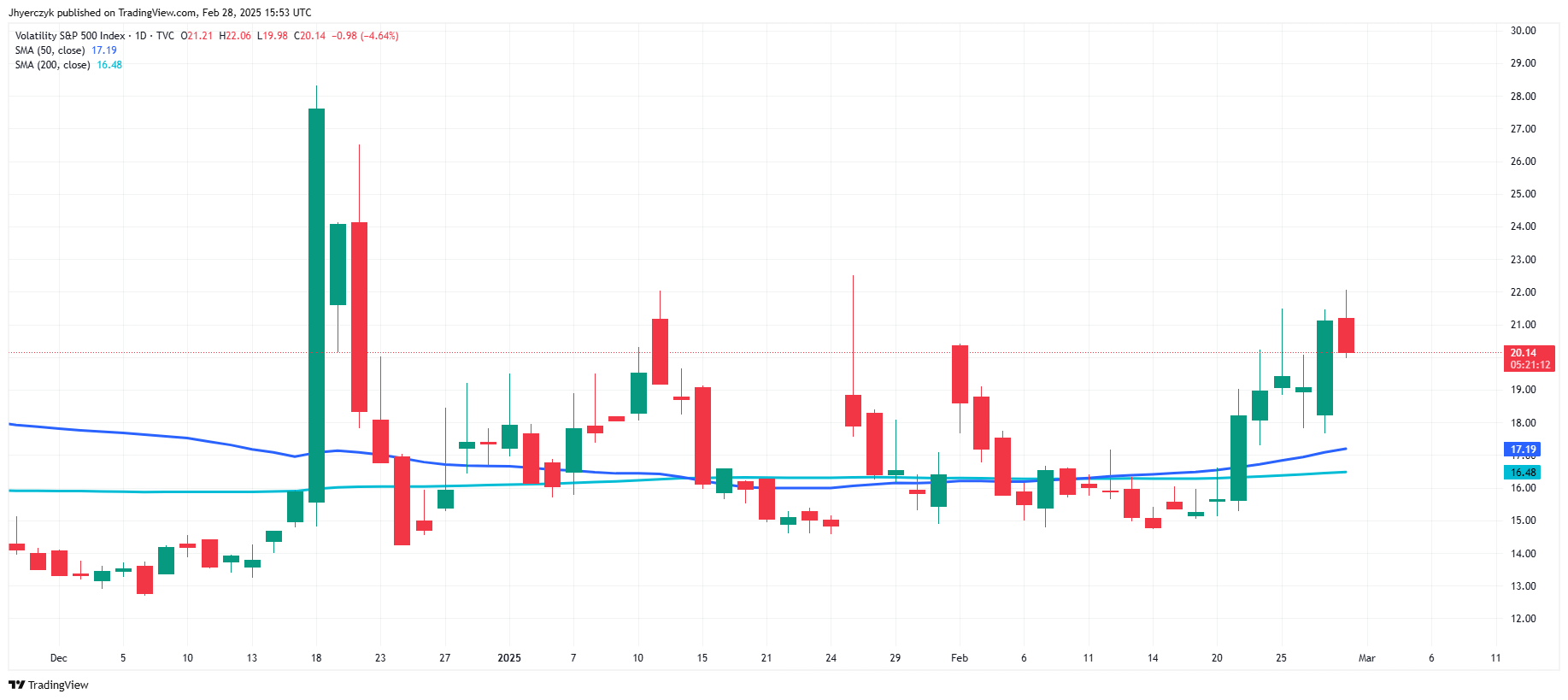

Daily Volatility S&P 500 IndexThe CBOE Volatility Index (VIX), Wall Street’s “fear gauge,” hit a one-month high, rising to 21.26 points, underscoring the market’s jittery sentiment.

Tech Under Pressure: What’s Driving Declines?

Tech heavyweights faced selling pressure. Nvidia slid 1.9% following an 8.5% drop on Thursday, as its weaker-than-expected gross margin outlook overshadowed a positive revenue forecast. Dell and HP Inc. also suffered, falling 5.7% and 6.6%, respectively, due to disappointing margin and profit forecasts.

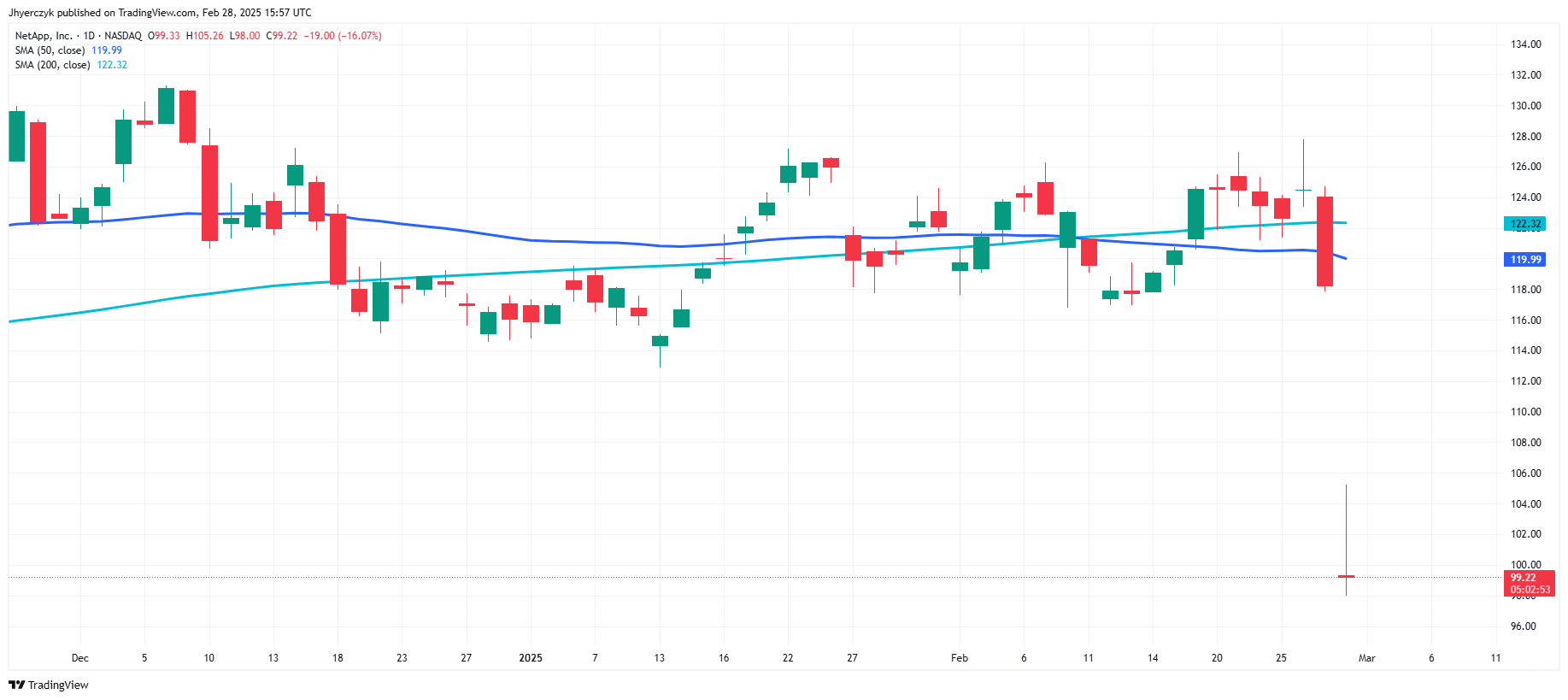

Adding to the tech sector’s woes, NetApp plunged 11.3% after cutting its annual outlook, while Walgreens dropped 4.8% on news that Sycamore Partners might acquire the pharmacy chain.

Market Outlook: What Should Traders Watch Next Week?

Looking ahead to Monday and beyond, traders should brace for continued volatility as the market digests mixed economic signals. The S&P 500 is on track for its biggest monthly decline since April 2024, and the Nasdaq is nearing its worst month since September 2023, suggesting potential for more downside pressure.

Key catalysts next week include Federal Reserve commentary, particularly from Fed Chair Jerome Powell, and fresh economic data, including the ISM Manufacturing Index and the monthly jobs report. Any signs of labor market softness could bolster expectations for a rate cut, potentially lifting risk assets.

Additionally, geopolitical developments, including potential new tariffs on Chinese goods, could impact sentiment, particularly in sectors exposed to international trade. With defensive sectors outperforming, traders might look to rotate into consumer staples and utilities for stability, while remaining cautious on high-valuation tech stocks facing margin pressures.

Overall, a cautious, data-driven approach will be critical as the market seeks direction in the face of rising recession risks and ongoing inflationary pressures.

More Information in our Economic Calendar.

About the Author

James HyerczykProfits & Punchlines

Mr.Hyerczyk is a technical analyst, market researcher, educator and trader. Jim is an expert in the area of patterns, price and time analysis, Forex and stocks.

Latest news and analysis

Advertisement