Advertisement

Advertisement

U.S. GDP Contracts 0.5% in Q1 as Inflation Rises and Consumer Spending Slows

By:

Key Points:

- U.S. GDP shrank 0.5% in Q1 2025, reversing Q4 growth, driven by rising imports and slowing consumer spending.

- Consumer spending was revised lower, contributing to a 1.9% rise in final sales—down from 2.5% in the previous estimate.

- Inflation ticked higher with core PCE at 3.5%, reinforcing the Federal Reserve’s cautious policy stance.

U.S. GDP Contracts 0.5% in Q1: Imports, Government Spending Drag Down Output

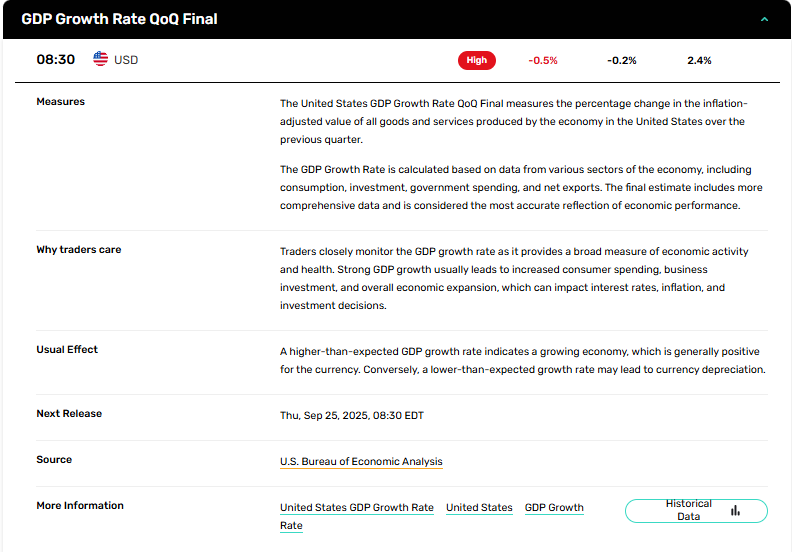

The U.S. economy contracted at an annualized rate of 0.5% in Q1 2025, according to the Bureau of Economic Analysis’ third estimate—marking a significant reversal from Q4 2024’s 2.4% growth. This downward revision reflects weaker-than-expected consumer spending and exports, raising concerns over the near-term economic outlook for traders.

Consumer Spending and Exports Miss Expectations

The downward revision of 0.3 percentage points from the second estimate was driven largely by slower consumer spending and softer exports. Consumer outlays—critical to U.S. growth—showed reduced momentum, contributing to the revised 1.9% increase in real final sales to private domestic purchasers, down from the previous 2.5%. Despite increased investment, demand weakness and a sharp rise in imports, which subtract from GDP, weighed heavily on overall output.

Goods Sector Under Pressure as Services Hold Ground

Industry data revealed a notable 2.8% contraction in real value added for private goods-producing industries, underscoring weakness in manufacturing and industrial activity. Private services-producing industries saw a mild 0.3% decline, while government value added grew 2.0%, partly buffering the broader decline. Real gross output eked out a 0.6% gain, driven by a 1.1% rise in services, as goods output and government contributions each slipped 0.6%.

Inflation Estimates Revised Higher; GDI Shows Resilience

The PCE price index was revised up to a 3.7% gain, while core PCE (excluding food and energy) climbed 3.5%, both 0.1 percentage point higher than prior estimates. This upward inflation revision supports the Federal Reserve’s cautious stance, limiting the case for near-term rate cuts. Meanwhile, real gross domestic income (GDI) rose 0.2%, reversing the prior -0.2% estimate and offering a more balanced view of economic activity.

Corporate Profits Decline but Less Than Feared

Corporate profits fell by $90.6 billion in Q1 but were revised up by $27.5 billion from the previous estimate. While still negative, the smaller-than-expected drop suggests firms are under pressure but not collapsing. The revised earnings data may soften bearish sentiment in equity markets, particularly within the S&P 500’s industrial and consumer sectors.

Market Forecast: Bearish Near-Term Bias

With GDP contracting and inflation readings firming, traders should expect short-term bearish pressure on equities and potentially volatile bond market behavior. The Federal Reserve is unlikely to pivot dovish until inflation cools further. Watch for sector rotation as investors reassess consumer and industrial exposure heading into Q2.

About the Author

James HyerczykProfits & Punchlines

Mr.Hyerczyk is a technical analyst, market researcher, educator and trader. Jim is an expert in the area of patterns, price and time analysis, Forex and stocks.

Advertisement