Advertisement

Advertisement

UK Inflation Softens Across Key Metrics; GBP Falls

By:

GBP Lower on softer UK inflation data.

In this article:

According to a report released by the Office for National Statistics (ONS) this morning, UK inflationary pressures in September eased across all key indicators. This, of course, will be welcomed news for the Chancellor of the Exchequer, Rachel Reeves, as she prepares to deliver her first Annual Budget at the end of the month.

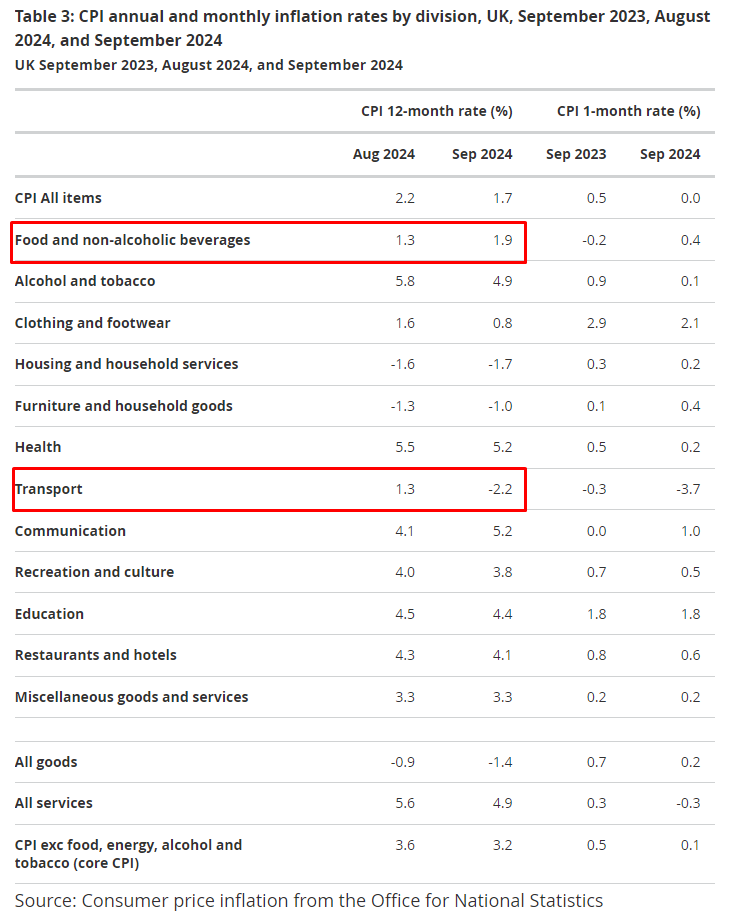

CPI Inflation Dips Below BoE Target

Headline CPI inflation (Consumer Price Index) slowed to 1.7% (YoY), touching a three-year low and was comfortably lower than the 2.2% reading in August. Opening the door for the Bank of England (BoE) to become a ‘bit more aggressive’ with easing policy, this positions the headline metric below the BoE’s inflation target of 2.0% (first time since April), as well as beneath recent BoE projections (August) and comfortably south of market estimates of 1.9%. Per the BoE’s latest projections, CPI inflation is expected to remain above 2.0% in 2025 and fall below target in 2026.

ONS chief economist Grant Fitzner commented: ‘Lower airfares and petrol prices were the biggest driver for this month’s fall. These were partially offset by increases for food and non-alcoholic drinks, the first time food price inflation has strengthened since early last year’.

Excluding energy, food, alcohol and tobacco, core (YoY) inflation cooled to 3.2%, easing from 3.6% in August (market consensus: 3.4%). Regarding services – a measure that the BoE monitors closely – YoY inflation came in at 4.9% versus 5.2% expected and 5.6% in August. This is quite the drop and represents the first time in over two years that this measure has been south of 5.0%.

GBP on the Ropes

Following the lower-than-expected inflation data, the GBP (British pound) saw a reasonably strong downside move, with FTSE 100 futures higher. Thirty minutes following the release, the UK government bond market (Gilts) opened with a moderate dovish rate repricing to 24 basis points (bps) of easing compared to 20bps of cuts before the release. This assigns a 90% probability that the BoE will reduce policy by 25bps at 7 November meeting. Following the open, there was some extension to the downside in the GBP.

However, while a rate cut is on the table for November, strengthened by comments from BoE Governor Andrew Bailey in September – communicating the central bank could become ‘more aggressive’ and a ‘bit more activist’ in easing policy should inflation continue to subside – ‘the upcoming budget is seen as the final hurdle’, according to Suren Thiru, Economics Director at ICAEW. Thiru added: ‘Rate setters will want to assess the inflationary impact of any measures announced before loosening policy again’.

Technically, the GBP/USD is testing key support on the daily chart at US$1.2994. The FP Markets Research Team recently noted, ‘this support level is positioned directly south of the higher low formed on 11 September at US$1.3002, and whipsawing below this base would likely trip stops and provide liquidity (sell orders) for longs at US$1.2994’. The concern for some investors will be price action on the monthly chart navigating below support from US$1.3111.

DISCLAIMER:

The information contained in this material is intended for general advice only. It does not take into account your investment objectives, financial situation or particular needs. FP Markets has made every effort to ensure the accuracy of the information as at the date of publication. FP Markets does not give any warranty or representation as to the material. Examples included in this material are for illustrative purposes only. To the extent permitted by law, FP Markets and its employees shall not be liable for any loss or damage arising in any way (including by way of negligence) from or in connection with any information provided in or omitted from this material. Features of the FP Markets products including applicable fees and charges are outlined in the Product Disclosure Statements available from FP Markets website, www.fpmarkets.com and should be considered before deciding to deal in those products. Derivatives can be risky; losses can exceed your initial payment. FP Markets recommends that you seek independent advice. First Prudential Markets Pty Ltd trading as FP Markets ABN 16 112 600 281, Australian Financial Services License Number 286354.

About the Author

Aaron Hillcontributor

Aaron graduated from the Open University and pursued a career in teaching, though soon discovered a passion for trading, personal finance and writing.

Latest news and analysis

Advertisement