Advertisement

Advertisement

Dax Index News: German Factory Orders Surge as Markets Await Key US Jobs Data

By:

Key Points:

- DAX climbs 0.54% as corporate earnings lift sentiment.

- German factory orders rebound 6.9% in December, sparking hopes of economic recovery amid mixed Q4 trends.

- US Fed policy remains in focus as labor market data fuels uncertainty over potential rate cuts in H1 2025.

DAX Opens Higher on Corporate Earnings Sentiment

The DAX Index opened higher on Thursday, February 6, climbing 0.54% to 21,703 as investors focused on corporate earnings and central bank stances.

Siemens Healthineers, Societe Generale, and L’Oreal are among the big names due to release earnings results, influencing market sentiment.

Sector Performance: Infineon Tech and Siemens Healthineers Lead Gains

Infineon Technologies surged 5% after beating earnings estimates earlier in the week and raising its forward guidance. Siemens Healthineers gained 1.23% with corporate earnings in focus.

Meanwhile, the overnight rebound in US AI-linked stocks drove demand for Siemens Energy, which opened 0.81 higher.

German Factory Orders Show Signs of Recovery

Germany’s factory orders offered a glimmer of economic optimism on Thursday, February 6, surging 6.9% in December after tumbling 5.2% in November.

According to Destatis:

- Excluding large orders, incoming orders were 2.2% higher than in November.

- Despite December’s upswing in orders, the automotive industry reported a 3.2% slump in orders.

- Factory orders were unchanged in Q4 2024 compared with Q3 2024.

Destatis remarked on the order trends for 2024:

“In 2024 as a whole, new orders in the manufacturing sector were 3.0% lower than in the previous year, adjusted for calendar effects. In the first half of the year, the downward trend observed since 2021 continued, while in the second half of the year there were signs of stabilization.”

US Markets Recap

On Wednesday, February 5, US equity markets added to Tuesday’s gains on relief over the US administration’s restrained approach to tariffs. The Dow rose 0.71%, while the Nasdaq Composite Index and S&P 500 advanced by 0.19% and 0.39%, respectively.

In the bond markets, 10-year US Treasury yields slid to a Wednesday low of 4.4%, bolstering investor demand for riskier assets. President Trump’s relatively benign tariffs on China eased fears of surging US import prices and inflation, tempering expectations of a more hawkish Fed rate path.

US services sector data contributed to the drop in yields. The ISM Services PMI and ISM Services Price Index trended lower in January. As the main contributor to the US economy and inflation, January’s figures supported a more dovish Fed policy stance.

However, labor market data limited the market optimism toward a near term Fed rate cut. The ADP reported a 183k rise in employment for January after a 176k increase in December. Tighter labor market conditions could boost wages, fueling consumer spending and demand-driven inflation.

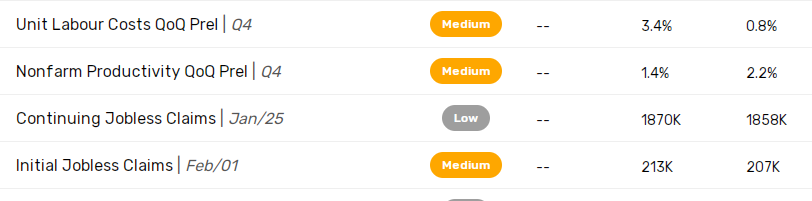

US Labor Market in Focus

Looking ahead to Thursday’s US session, the labor market will be in focus. Initial jobless claims, unit labor costs, and nonfarm productivity trends could influence the Fed rate path.

- Lower jobless claims and higher unit labor costs could lower expectations of an H1 2025 Fed rate cut.

- Conversely, an unexpected spike in jobless claims may boost demand for riskier assets on Fed rate cut bets.

Central bank rate paths influence borrowing costs, potentially affecting corporate earnings and valuations.

Investors should also monitor US-China and EU trade developments, which will be crucial for risk sentiment. An escalation in trade tensions could impact demand for risk assets, while progress toward trade deals may lift market sentiment.

Natixis Asia Pacific Chief Economist Alicia Garcia underscored US tariff risks, stating:

“Europe should ‘get ready’ for tariffs. He seems to be picking fights with those countries who are closer. The lower proposed duty on China was likely a result of Trump’s desire to strike a ‘deal’ of some kind with Beijing.”

Near-Term Outlook

The DAX’s trajectory hinges on upcoming German economic indicators, US labor market data, and central bank forward guidance.

- Weaker economic data and more dovish policy stances could drive the DAX toward its all-time high of 21,801.

- A tighter US labor market, upbeat German data, and more hawkish policy outlooks may pull the DAX toward 21,000.

Beyond the economic calendar, tariff developments could prove pivotal for risk sentiment. Ongoing threats of US tariffs on EU goods and retaliatory measures against China’s tariffs could impact global markets.

As of Thursday morning, US futures pointed to a positive session, with the Nasdaq 100 mini advancing by 28 points.

DAX Technical Indicators

Daily Chart

Despite ongoing US tariff uncertainty, the DAX sits well above the 50-day and 200-day Exponential Moving Averages (EMAs), sending bullish price signals.

If the DAX breaks above 21,750, the Index could climb toward its record high of 21,801 next. A break above 21,801 could pave the way for a move toward 22,000.

Conversely, a DAX drop below 21,500 could signal a fall toward 21,350. A fall through 21,350 may bring 21,000 into sight.

With the 14-day Relative Strength Index (RSI) at 71.32, the DAX sits in overbought territory (RSI higher than 70). Selling pressure may intensify at the morning high of 21,731.

Final Thoughts

The DAX’s direction hinges on tariff negotiations, central bank policy signals, corporate earnings, and economic data. Investors should monitor upcoming US labor market figures and earnings releases for further market cues. Trade-related developments remain a key risk factor, with any shifts in US-EU and US-China policies likely to affect sentiment.

Market sentiment remains on edge as corporate earnings, central bank signals, and trade policies shape the DAX’s next move. Stay ahead with our latest insights and real-time analysis here.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement