Advertisement

Advertisement

Dax Index News: German Inflation in Focus, Trump’s Trade War Risks DAX Gains

By:

Key Points:

- DAX hits record highs as ECB rate cuts and dovish guidance fuel bullish momentum, but inflation data may shift market sentiment.

- Trump’s tariff threats against BRICS nations raise concerns over global trade, adding risk to European markets.

- Investors eye German and US inflation data, with a lower-than-expected print potentially boosting ECB and Fed rate cut bets.

DAX Hits Record High on ECB Rate Cut and Forward Guidance

On Thursday, January 30, the DAX rose 0.41%, adding to Wednesday’s 0.97% gain, closing at a high of 21,727.

Softer-than-expected Euro area economic indicators supported a more dovish ECB policy stance to bolster the economy.

Sector Highlights: Siemens Energy and Vonovia Lead Gains

Siemens Energy AG extended its gains from Wednesday, rallying 4.04%. Upbeat Q1 revenue figures continued driving buyer demand.

Real estate firm Vonovia benefited from the ECB rate cut and dovish forward guidance, advancing by 3.13%.

Auto stocks contributed to Thursday’s gains amid US President Trump’s silence on EU tariffs. Notable movers included Daimler Truck Holding and Porsche, which rose 1.42% and 1.07%, respectively.

German Economy Contracts in Q4 2024

The German economy shrank by 0.2% quarter-on-quarter in Q4 2024 after growing by 0.1% in Q3 2024. The slowdown weighed on the Eurozone economy, which stalled in Q4 after expanding by 0.4% in Q3 2024.

Weaker-than-expected numbers enabled the ECB to signal a more dovish rate path, supporting demand for German-listed stocks.

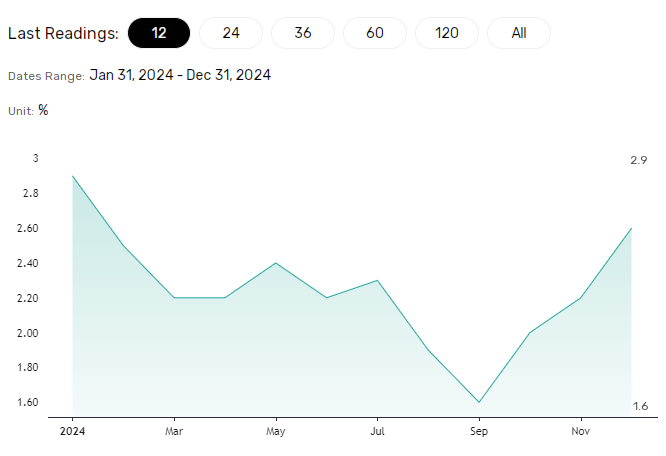

ECB Cuts Rates and Signals More Easing

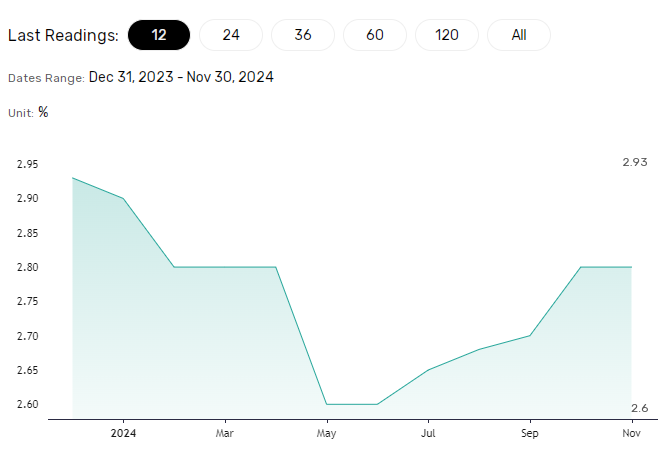

The ECB cut interest rates by 25 basis points to 2.9% on January 30. Significantly, ECB President Christine Lagarde signaled further economic weakness, increasing the chances of additional rate cuts.

Frederik Ducrozet, Head of Macroeconomic Research at Pictet Wealth Management, remarked on the ECB’s rate stance, saying,

“Most importantly for the ECB, confidence in the return of inflation to the target remains high as core inflation and wage growth normalise. Therefore bringing rates back to neutral (~2%) should be a no-brainer, at least as a first step.”

German Inflation in Focus

On Friday, January 31, German inflation figures could influence the ECB rate path. Economists expect the annual inflation rate to remain at 2.6% in January.

A higher inflation rate could temper bets on multiple ECB rate cuts, potentially weighing on rate-sensitive stocks. Conversely, a drop toward 2% may bolster expectations of aggressive ECB rate cuts. A dovish ECB rate path could drive the DAX higher as lower borrowing costs boost earnings and valuations.

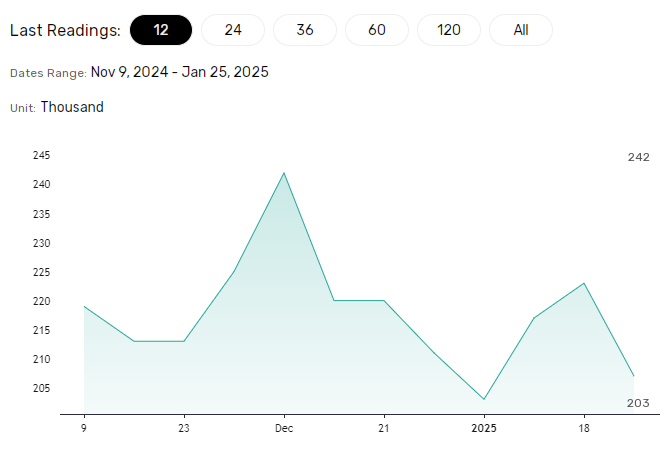

Other stats include Germany’s unemployment and retail sales figures. However, the inflation report will likely be the focal point.

US Economy Slows But Inflation Accelerates

On January 30, US economic indicators complicated the Fed’s policy outlook. The US economy grew by 2.3% quarter-on-quarter in Q4 2024 after expanding by 3.1% in Q3 2024. A weaker economy could support the case for a near-term Fed rate cut.

However, inflation and labor market data supported Fed Chair Powell’s warnings against cutting rates. The Core PCE Index rose by 2.5% quarter-on-quarter in Q4 2024, up from 2.2% in Q3 2024. Initial jobless claims trended lower, reflecting a resilient labor market.

A more hawkish Fed rate path could raise borrowing costs, affecting demand for riskier assets.

US Markets Trend Higher on Earnings

US equity markets ended January 30 in positive territory, driven by corporate earnings and economic indicators. The Nasdaq Composite Index rose 0.25%, while the Dow and the S&P 500 gained 0.38% and 0.53%, respectively.

Tech giant Microsoft (MSFT) slid by 6.18% after warning its cloud business would miss third-quarter forecasts. Meanwhile, Tesla (TSLA) rallied 2.87% after CEO Elon Musk promised to launch cheaper models in H1 2025.

US Economic Calendar: Personal Income and Outlays Report in Focus

On January 31, traders must consider the Personal Income and Outlays Report, crucial for the Fed. Economists expect the Core PCE Price Index to rise 2.8% year-on-year in December, similar to November’s increase.

A pickup in inflationary pressures could sink bets on an H1 2025 Fed rate cut, impacting demand for riskier assets. Conversely, a softer inflation reading may rekindle bets on a near-term Fed move, potentially driving the DAX to record highs.

Other stats include personal income and spending figures. These may also influence sentiment toward the Fed rate path as they are leading inflation indicators.

Near-Term Outlook

The DAX’s performance will depend on German and US inflation.

- Softer inflation figures could drive the DAX toward 22,000.

- Higher inflation could affect sentiment, potentially dragging the Index below 21,500.

External factors, including potential stimulus from Beijing and US tariffs, will influence DAX trends. Chinese stimulus could support German exports, while US tariffs may create headwinds.

As of Friday morning, futures signaled a mixed start to the session. DAX futures were down 13 points, while the Nasdaq 100 mini jumped 112 points. The DAX pulled back after reports that Trump threatened BRICS nations with 100% tariffs if they shifted away from the US dollar.

DAX Technical Indicators

Daily Chart

After a three-day winning streak, the DAX sits well above the 50-day and 200-day Exponential Moving Averages (EMAs), affirming bullish price signals.

A break above the January 30 record high of 21,732 could enable the bulls to target 22,000. A breakout from 22,000 may bring the 22,500 level into play.

Conversely, if the DAX falls below 21,500, it could test the key support level at 21,000.

With the 14-day Relative Strength Index (RSI) at 79.52, the DAX remains in overbought territory (RSI higher than 70). Selling pressure could intensify at Thursday’s record high of 21,732.

Conclusion: Key Drivers to Watch

Traders should monitor upcoming German and US economic indicators. External factors, including Chinese economic policies and US tariff developments, could further influence the DAX’s trajectory.

Read our detailed analysis of how global market dynamics influence the DAX’s performance here.

About the Author

Bob MasonChief Crypto Boss

TEST 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Latest news and analysis

Advertisement