Advertisement

Advertisement

Dax Index News: Bank Stocks Lifted by ECB, But Trade Risks Cloud DAX Forecast

By:

Key Points:

- The DAX ended its 3-day rally, slipping 0.08% on June 6 as weak German data and ECB hawkishness spooked investors.

- German exports fell 1.7% in April, while US-bound shipments plunged 10.5%, raising trade war concerns.

- DAX outlook now hinges on US inflation data, ECB signals, and US-EU trade negotiations due this week.

DAX Snaps Three-Day Winning Streak

The DAX slipped 0.08% on Friday, June 6, partially reversing Thursday’s 0.19% to close at 24,305. Notably, the index snapped a three-day winning streak.

Weak economic indicators and Thursday’s more hawkish-than-expected ECB press conference pressured the index at the opening bell. German exports slid 1.7% month-on-month in April. Exports to the US plunged 10.5%, reflecting the potential impact of lingering tariffs on the German and Euro Area economies. Meanwhile industrial production fell 1.4% in April.

Daniel Kral, a Europe macro specialist at Oxford Economics, commented on Friday’s data, stating:

“Predictably Germany’s industrial production sank in April, giving up most gains from the US inventory build-up the previous month. Uncertainty and weak demand weigh on the near-term but leading indicators point to green shoots as fiscal stimulus and defence spending will kick in.”

Bank Stocks Advance on Hawkish ECB Cues

Bank stocks extended their gains on expectations of a less dovish ECB stance. Deutsche Bank rose 0.71%, while Commerzbank advanced 0.18%.

By contrast, Trump’s steel and aluminum tariff hike and lack of progress toward a US-EU trade deal weighed on auto stocks. Volkswagen dropped 1.72%, with Porsche, Mercedes-Benz Group, and BMW also posting losses.

Wall Street Rallies on Strong US Jobs Report

US markets reversed their losses from June 5 as the market focus turned from the President Trump-Elon Musk feud to the US labor market. A solid US Jobs Report eased recession fears, boosting demand for risk assets. The Nasdaq Composite Index rallied 1.20%, while the Dow and the S&P 500 gained 1.05% and 1.03%, respectively. Notably, Tesla (TSLA) shares climbed 3.67%, only partially reversing Thursday’s 14.26% plunge.

Average hourly earnings rose 3.9% year-on-year in May, matching April’s trends. A 139k increase in nonfarm payrolls left the unemployment rate steady at 4.2%. However, the participation rate unexpectedly dropped, suggesting some underlying weakness in the labor market.

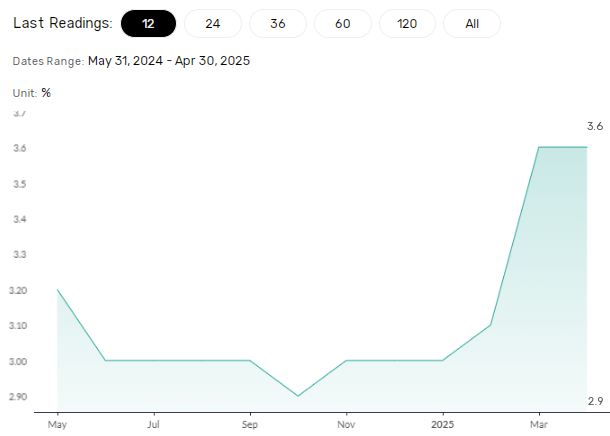

Consumer Inflation Expectations in Focus

Later in the European session on Monday, June 9, US consumer inflation expectations will draw interest. Economists forecast consumer inflation expectations to hold steady at 3.6% in May.

A softer reading may raise bets on a Q3 2025 Fed rate cut, boosting demand for risk assets, including the DAX. Conversely, a higher reading could support the Fed’s wait-and-see stance, weighing on risk sentiment. Markets might be more sensitive to the data as the upcoming US CPI Report (due on June 11) could swing sentiment toward the Fed’s policy stance.

Could Trade Talks Trigger a DAX Breakout?

Traders should also monitor US-EU trade developments. Progress toward a trade deal may impact the ECB’s stance on a July rate cut. Failed talks may revive hopes for a July rate cut, raising demand for DAX-listed stocks.

Frederik Ducrozet, Head of Macroeconomic Research at Pictet Wealth Management, commented on the potential effects of tariffs on the Euro Area GDP and ECB rate path, stating:

“ECB staff projections with trade shocks: in a severe trade war scenario, GDP is 1% lower and inflation down to 1.8% in 2027, calling for more rate cuts. A mild scenario implies stronger growth and stable inflation, with the ECB likely on hold.”

Outlook: Key Catalysts for the DAX

The DAX’s near-term trajectory hinges on the US inflation, US-EU trade developments, and central bank commentary.

- Bullish Case: Positive US-EU trade developments, softer US inflation, and dovish central bank signals could send the DAX toward 24,500.

- Bearish Case: A breakdown in trade talks, stronger-than-expected US inflation, or hawkish central bank commentary may pull the DAX toward 24,000.

As of Monday morning, the DAX futures were flat, while the Nasdaq 100 mini dropped 30 points, signaling potential for a volatile start to the week.

Technical Setup Suggests Cautious Optimism

Despite Friday’s loss, the DAX remains above the 50-day and the 200-day Exponential Moving Averages (EMA), signaling underlying bullish momentum.

- Upside Target: A breakout above the June 5 record high of 24,479 could pave the way to 24,750, with 25,000 level the next key psychological resistance level.

- Downside risk: A break below 24,000 brings 23,750 into play, followed by the May 23 low of 23,275 as the next support level.

The 14-day Relative Strength Index (RSI), at 65.38, suggests the DAX has room to retest 24,479 without entering overbought territory (RSI > 70).

Conclusion: Eyes on Inflation, the ECB, and Trade News

Traders should closely monitor US-EU trade developments, upcoming US inflation data, and ECB signals for guidance.

Explore our exclusive forecasts to assess whether improving trade sentiment could lift the DAX to new highs. Refer to our latest forecasts and macro insights Forecasts for further analysis, and consult our Economic Calendar.

About the Author

Bob MasonChief Crypto Boss

123456789 30 He has written extensively for a broader audience and his current focus is on developments relating to the financial markets including, but not limited to currencies, commodities, alternative asset classes, and global equities.

Advertisement